Is the Reverse Repo drainage about to blow up the credit markets? Adam Taggart / Lance Roberts Interview Notes 12/08/23

12/14/2023

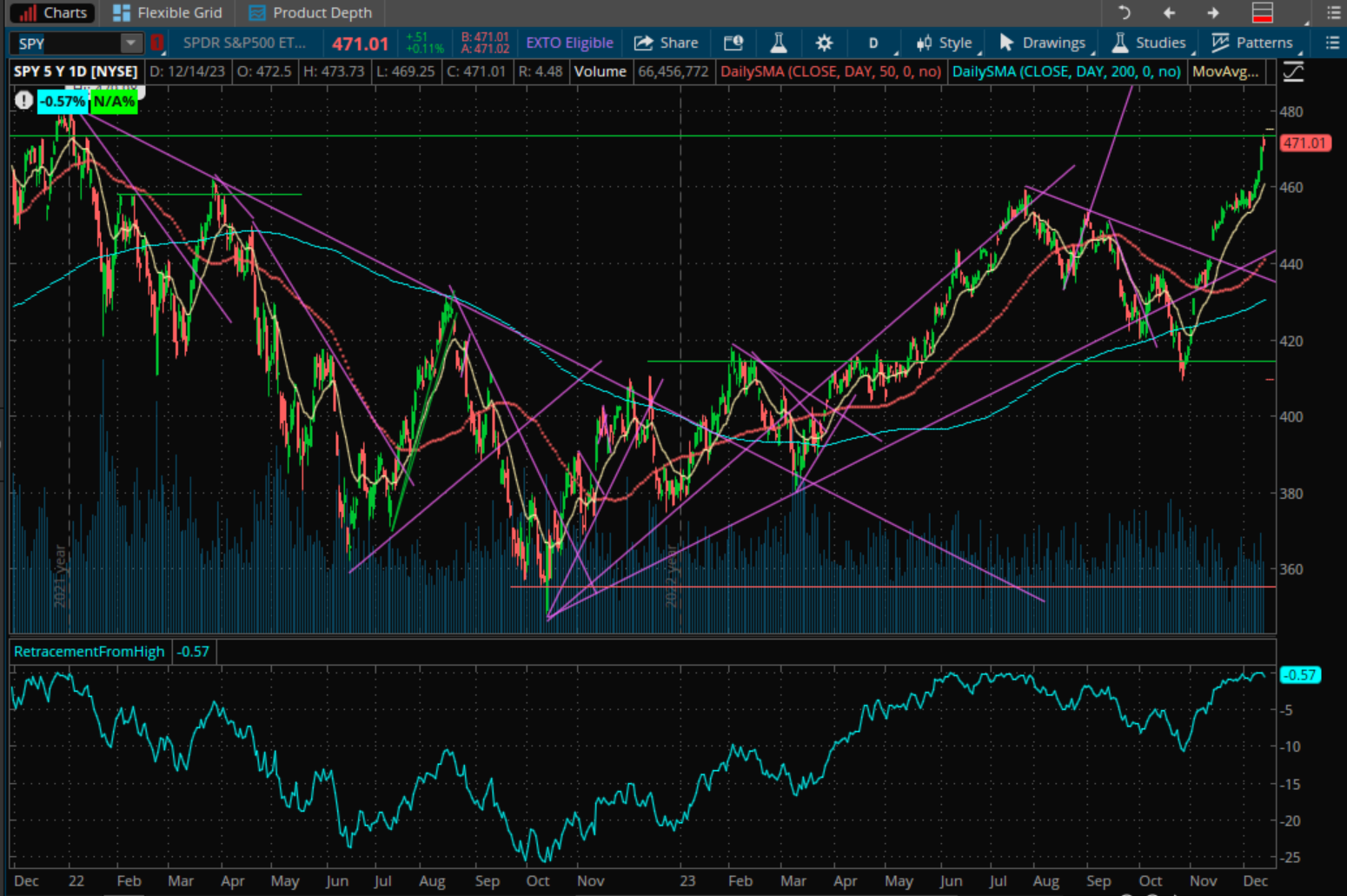

2:45 - How will the market digest current overbought conditions? Previously, Lance stated that he expects a pullback, or some grinding sideways before the market continues uptrend.

Market has been trading sideways for a few days, sees a MACD sell signal. Doesn't mean a selloff is coming, just the upside is contained.

Greenspud: Lance's chart displayed above precedes a strong upside rip in the market that occurred in concert with the FOMC meeting during the week.

7:30 One of the best Novembers EVER for stocks. Did we pull the "Santa Claus" rally forward?

Probably yes to some degree. Depends on what the market does over the next couple of weeks. If correction happens, then it gives the market better ability to rally into the year end for fund window dressing. If stocks go up, doesn't necessarily preclude a year-end advance, just limits it.

"Santa Claus rally" is last 5 days of December and first few days of January.

Lance: expecting a little bit of a pullback. Used the current rally to raise a little bit of cash. Got rid of losers for tax loss selling. Repositioned portfolio.

We will get a correction at some point. Question is from where will that correction be and where it goes to.

11:00 Is Lance "less confident" of a Santa Claus rally?

Still thinks we will get a SC rally. The matter is how much of a degree it will be.

Greenspud: To me this "Santa Claus rally" is such a narrowly defined, specific statistical expectation that I'm not really thinking about it much. I just look at the charts and see what the current setups tell me. Trying to catch a Santa Claus rally doesn't interest me.

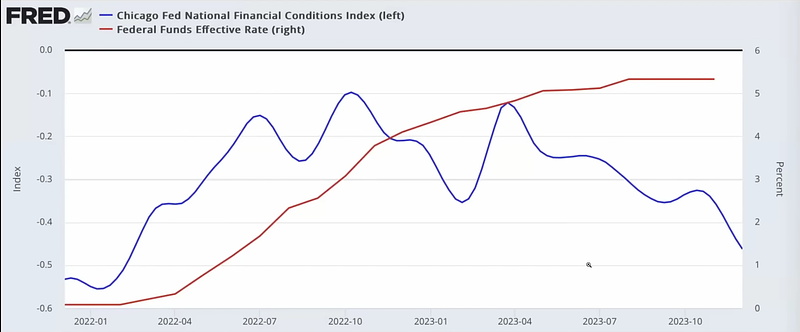

16:00 Disconnect between monetary policy and financial conditions.

Jerome Powell said in October: stocks and bonds going down is doing their job for them (i.e. bearish sentiment in the markets will lead to a slowing of economic activity due to expectations, so rate hike becomes less necessary)

Lance thinks that Powell will stick with the stance that rate hikes can continue. (Then it must have been a big surprise when the FOMC hinted at possible 3 rate cuts in 2024.)

Investors are trained to buy every dip for the past 13 years. FOMO -> causes a rush to try to catch the bottom.

23:00 Adam thinks the disconnect between Chicago Fed Financial conditions index and monetary policy could be about net liquidity flows. We had the BTFP launch early in the year. The Reverse Repo market getting drained. Could there just be more shadow liquidity?

On the Chicago Fed Financial Conditions Index: "The Chicago Fed’s National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets, and the traditional and “shadow” banking systems. Positive values of the NFCI have been historically associated with tighter-than-average financial conditions, while negative values have been historically associated with looser-than-average financial conditions." Source: Chicago Fed

Adam - will financial conditions have to tighten from here in order for Powell to win the inflation battle, stop campaign of interest rate hikes?

Plenty of liquidity still in the system. People spending. Money sitting in money market accounts for now. Federal expenditures high - we are running a $2T deficit. All this government spending is feeding economic growth.

M2 money supply as a percentage of GDP is still extremely elevated.

We don't know whether the slowdown will occur in 2024, 2025, 2026 because we keep finding new ways to spend. Consumers are very adept at finding new ways to get money. Buy now, pay later an example.

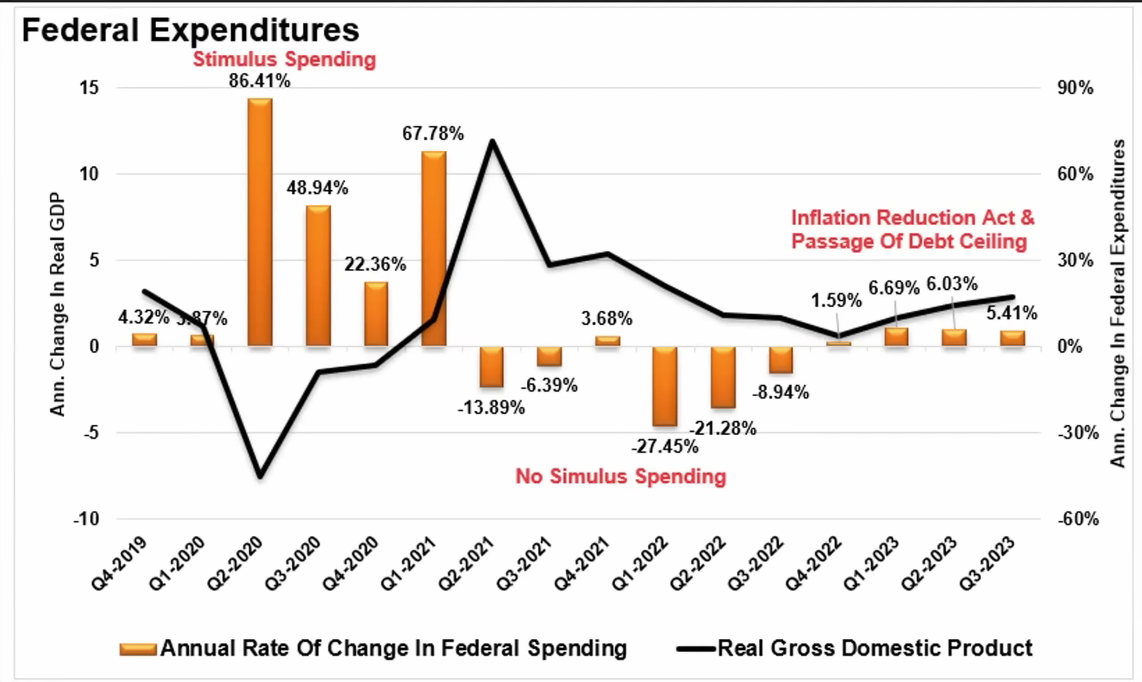

30:30 - What happens to bond yields next year? Are we already in a recession? Or can the consumer be stronger for a lot longer? Daniel DiMartino Booth more worried about deinflation - consumer spigot shut off and Federal expenditures getting harder because of a divided Congress. Wolf Richter says we need a recession but doesn't see it in the data because the consumer is doing well.

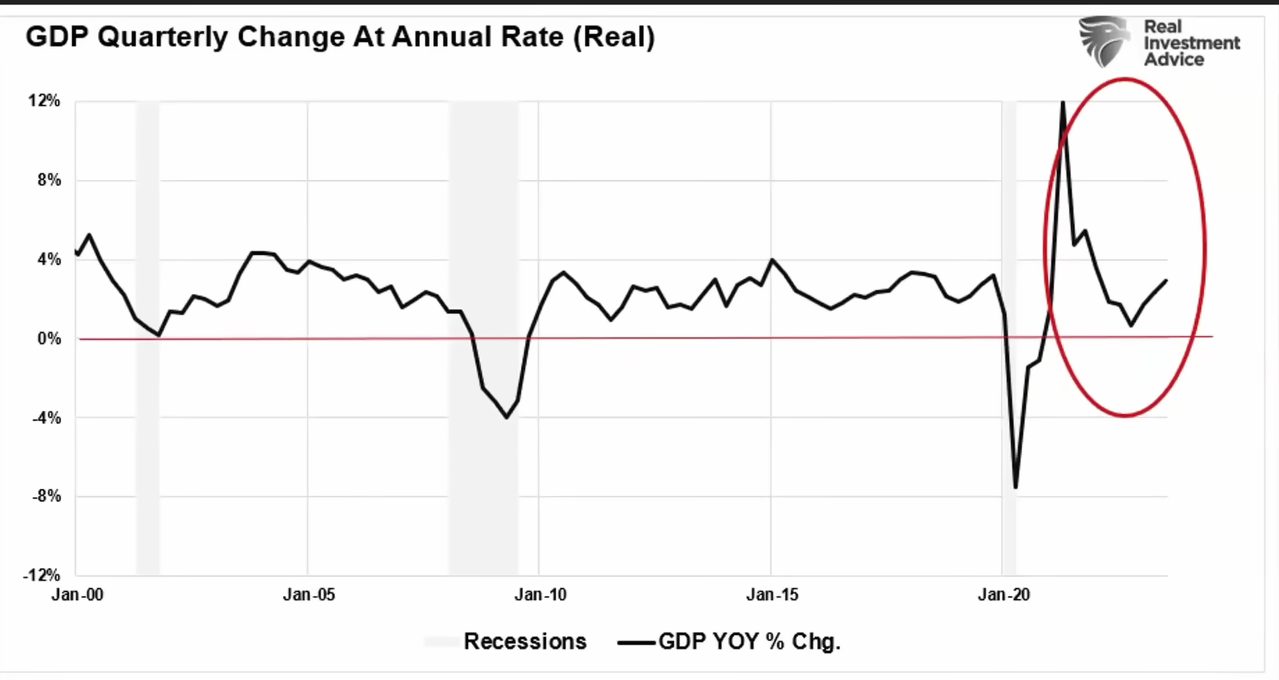

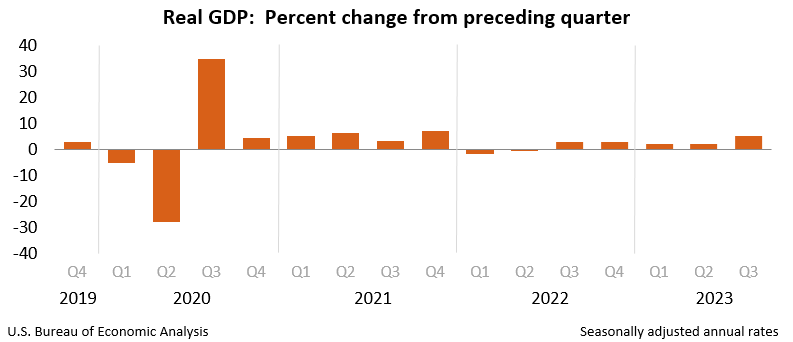

2020 was so abnormal - created an artificial recession by shutting down the economy and then flooding households with cash. The data is very badly skewed.

In the chart above, GDP jumped 12% because of the influx of liquidity from pandemic stimulus. It's almost fully reverted. In any other circumstance a 12% drop in GDP growth would be a big deal, but we started from such a high level of GDP growth with that 12% spike that it doesn't look like an actual recession because there's not a contraction of economic activity, but would be considered a dramatic slowdown in normal conditions. That spike really skews the interpretation of the data.

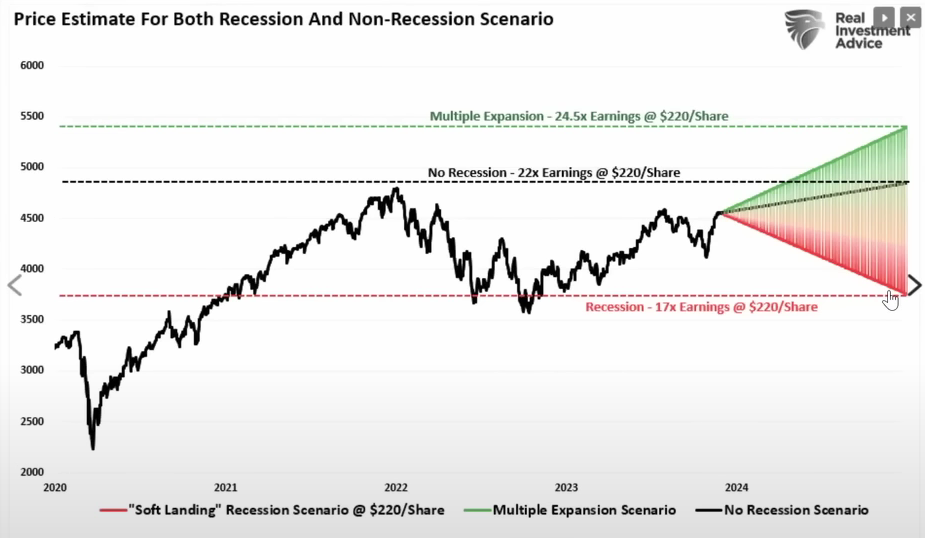

Zulauf: Thinks the markets will power higher in Q1 because of all the liquidity in the system. We might see S&P at 5000. Lag effects will eventually catch up. Sees a 40% correction potential in the S&P.

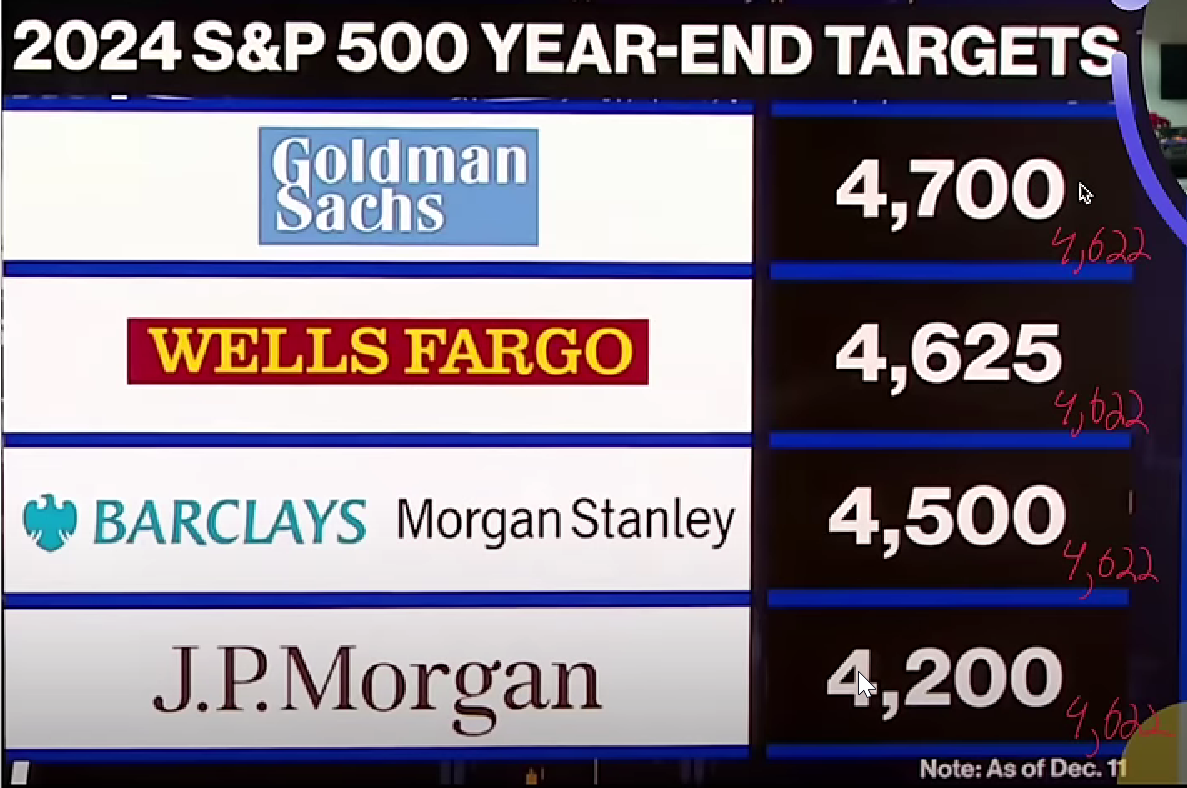

Lance: Looking at next year analysts are optimistic. Analysts are always paid to be optimistic because they benefit from selling investment services. In 2021-2021, Goldman said that market would climb 9% to 5100. Year actually ended at 3900.

Lance: The only question that matters is: How to structure your portfolio to navigate this range of possible outcomes>

57:30 Have we seen the peak in bond yields?

Zulauf: thinks we have hit the peak, could get as low as 3% by the end of next year. But not going big on the bond trade because he sees uncertainty in that.

Lance: Thinks the peak is in. Not enough of a driver to push yields to 5%. Inflation and economic growth pushes yields up. When yields were at 5%, that was overvalued in relation to inflation.

Lance is closing out some of his personal bond position since yields have come down so fast. Expecting FOMC to not be ready to cut rates yet. (Given it's now past the Wednesday announcement, this was an incorrect assumption.)

Lance: If Fed intervenes in the economy, worried about inflation, yields could go to 1%.

Zulauf says yields will go to the moon because of fiscal situation. Lance disagrees - 2010-2013 had $43T of government stimulus, but the only one that created inflation was checks to households. As long as rates are kept to 0% and QE, long term rates will stay low. Only thing that changes this is the Fed doing more "MMT" (Modern Monetary Theory - giving money to households)

1:03:00 - Reverse Repo Market - has been providing liquidity to system. At the rate that its being drained, should be empty by Q1 of next year. How substantial is that?

It's an issue but not a big one. If the Fed becomes more dovish, it will be because the Fed sees something in the credit markets that we don't see. If they come out at next FOMC meeting, then they are probably worried about this, there's stress in the financial system. Greenspud: Uh oh, this is exactly what happened!

When the Fed starts cutting rates, you don't wanna be long stocks. You wanna be long when the Fed STOPS cutting rates.

Daniel DiMartino Booth - Reverse repo has been an offset to the Fed's QT. When it goes away, then the full effect of QT will start to be felt.

1:08:00 Penalty for underpayment of Federal taxes has more than doubled over the past two years. Used to be 3% now it's 8%. As we are heading into the end of the year, one thing you should be looking at closely is estimated tax payments especially if you are a gig employee.

1:09:00 Lance's trades: none this week. Just waiting for the market to give us some kind of correction to buy into.

1:10:00- Discussion on "The American Dream" and young people's views on capitalism vs socialism.