The coming stagflation conundrum - Adam Taggart Thoughtful Money / Michael Pento notes 12/4/2023

12/05/2023

I closely watched Michael Pento's previous interviews on Wealthion and other shows like this. He's been bearish since at least 2022 and has had a consistently negative outlook on the US economy - much like a lot these interview guests.. As knowledgeable as many of these commentators are, it's easy to get scared out of investing entirely by what they have to say, so I go into an interview like this with a little skepticism.

In this interview Michael Pento was very straightforward in explaining why his 2023 predictions failed to materialize. He highlights some systemic monetary system issues that he believes will lead to a prolonged period of inflation coupled with low real returns on investments. But, he has a strategic plan for coming out ahead through all the chaos.

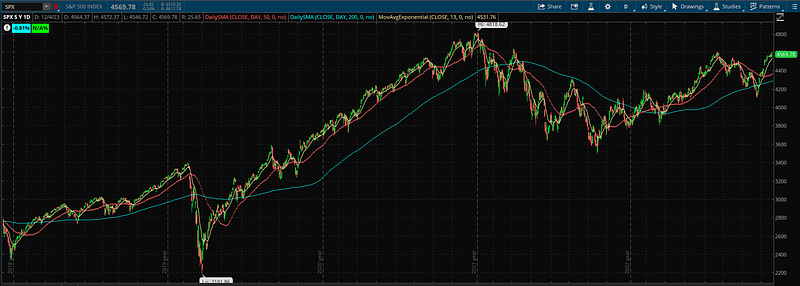

1:50 Bull market ended in late 2021

MP: "I don't believe the hype from the mainstream financial media. There will be no soft economic landing. And we are not in a bull market now and will not be in a bull market next year [2024]." Some facts:

The bull market ended in late 2021. The S&P 500 is still down 4% since its peak in November of 2021. Inflation adjusted, the shortfall is much worse.

There are 7 AI related stocks, up 80% in 2023. The other 493 stocks are up 4% for 2023. That's after being down 20% in 2022.

I think he's very much right about that. The market feels like it's been a bull, but it's just recovered territory from 2021. If you were a long term investor in the S&P500 at the 2021 and didn't add anything (let's say maybe you don't have the excess income), then you're not even back to breakeven.

The "bull", or more realistically, the "recovery" of 2023 reminds me a lot of the 2000 - 2008 period where the market had a huge decline from the post-9/11 recession, and then just as it recovered it got smacked down by an even worse fall with the 2008 financial crisis. My dad's retirement portfolio was near fully invested into the 2001 peak. He did not live long enough to see the market hit new highs again.

The Russell 2000 is down 27% since November 2021. The 60/40 portfolio, which includes bonds, is down 40% since 2022. (I don't know if he's citing a specific benchmark here.)

3:37 The salient issues have not been resolved.

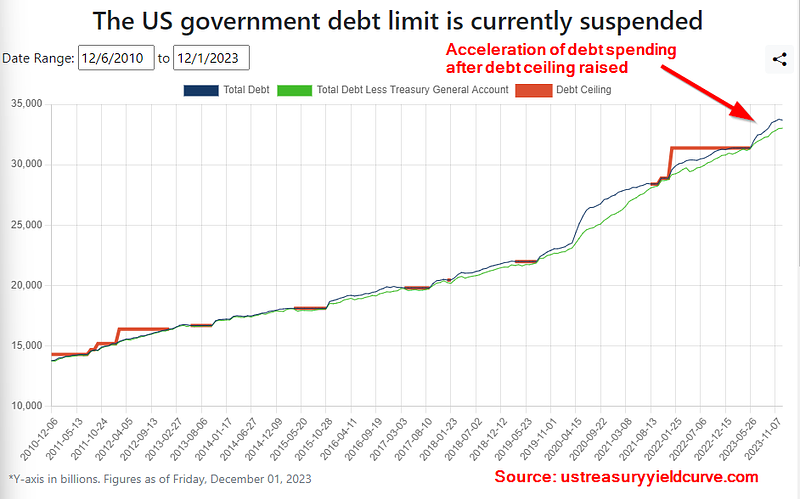

All problems stem from this: We had a sub-1% fed funds rate for 11 of the 14 years from 2008 to 2022. That led to a massive amount of cumulative debt, unserviceable amount of debt (especially under a "normal" interest rate regime), and unsustainable asset bubbles.

A crash is still coming, the timing is crucial, and MP will use his models for that timing.

MP: "I have not been net short in my portfolio for the entire duration of 2023. Not one day. I expected the recession to start....and it hasn't officially begun yet."

MP: "When the recession officially begins, the average decline in the S&P500 is 32%." according to historical data going back to the Great Depression. Expecting that to come in 2024.

"I was wrong about a 2023 recession, but not so wrong because in general the market hasn't gotten anywhere. The real economy is teetering on a collapse."

5:40 Magnificent 7 stocks - Fred Hickey is bearish on them (esp Apple and Tesla). Will they continue next year?

MP: History - whenever you see a concentration of stocks (cites the "nifty fifty" as an example), a very narrow group of stocks holding up the market it never ends well. "You can't have a healthy market with only a few stocks participating."

The equal weight S&P500 is down 10%, including the AI stocks.

Believes AI is the technology of the future, looking forward to investing in it, but does not believe it will be enough to save the stock market or the economy.

Anticipates earnings miss in the S&P 500.

"If you play this carefully, and you get your timing right, there's a tremendous amount of money to be made shorting this market, and going long the bond market Treasury complex in the correct duration."

"After this consummation of this reconciliation of the asset bubble occurs, that includes real estate as well, there's a tremendous opportunity to get long what I think is going to be a protracted period of stagflation such as this country has never seen before."

9:06 AT: Many people he's interviewed were wrong about the 2023 timing for a recession. MP was one of the first to make a recessionary call in 2022. Reasons for the incorrect timing are multi-factor.

AT: Refers to MP previously stating that the country will be facing the biggest monetary cliff and the biggest fiscal cliff happening simultaneously. We got the monetary cliff - QE turned off, Fed aggressive tightening. Reserves and BTFP alleviated the tightening, making it less aggressive. We didn't get the fiscal cliff. The fiscal side of the house still stimulating hard with deficit spending.

MP: 2 reasons recession delayed, but not cancelled. #1: Massive fiscal stimulus per Biden administration. #2: terms on the debt - fixed, long durations have been locked in (i.e. 30 year mortgages and corporate debt locked in at fixed rates) Over time debt will be refinanced at higher rates.

"I think the US debt is headed to junk status".

$34T debt - the interest is $700B, and will reach $1T by 2025. Entitlements and interest on debt will equal 100% of revenue by 2040.

Annual deficit is 45% of total revenue. National debt is 770% of annual Federal income.

Looking at debt as a percentage of income leads MP to the conclusion that the US government is insolvent.

Global debt: now $300T, 350% of global GDP. 26% higher than it was just prior to the 2008 financial crisis, when it was 278% of GDP. These rates are putting pressure on governments.

Central bank needs to monetize that debt (print money). But if you monetize, you have an inflation problem.

A long time ago I read the John Mauldin book Endgame which talked about debt monetization. After reading that book I always knew that hyperinflation was going to happen, it is just a matter of time. Governments love to spend but the long term cost of that debt is that they get rid of it by decrease it's value through inflation.

Corporations - $1.8T needs to be refinanced over the next 3 years. That carries an interest rate of 2.8%. Debt service payments are going to more than double next year.

40% of companies in the Russel 2000 are unprofitable right now. That was 20% heading into the 2008 financial crisis. The costs of borrowing has already doubled since 2022.

17:00 The illiquidity in the Treasury market is "eye popping". Let's see what happens in March of 2024 - $114B in BTFP funds are owed back. MP says his 2023 predictions were wrong because the Fed bailed everyone out [using the BTFP]. Banks will be getting the assets back on their balance sheets at even worse valuations than they were in March of 2023.

I think the fed is going to extend the BTFP. They aren't going to let that spark another financial crisis. The can will be kicked down the road some more.

20:00 Reverse repo facility runs dry in March of 2024. Banks are taking their excess reserves and buying Treasuries. Money is being taken out of the RRP and wiping out the base money supply through the QT program. By March 2024 there won't be any money left in the reverse repo facility, liquidity runs dry, and then the illiquidity in the Treasury market will go exponentially higher.

22:00 AT: Tries to sum of the root of the economic problems: "The biggest existential challenge is too much debt". Result of a fiat money system. They either have to let the bad monetary debts default, or inflate away the currency. Are we globally headed towards one of these two types of defaults? What's more likely?

MP: Likens it to a bully. They talk tough, but when punched in the face they back down. Central bankers talk tough about fighting inflation because their mandate is stable prices.

The worst thing that a central banker can create is a depression. The debt default route demands that a depression occurs.

When you take interest rates <1% for 11 years - that has never done before in the US - that creates massive economic distortions. 1) debt, 2) asset bubble (because we buy things with the debt, like homes)

$17T of negative yielding debt globally at the peak of this cycle. Leads to bubbles.

Bursting of the bond bubble is beginning. We haven't seen corporate debt burst yet, but that's coming in 2024. $1.8T corporate debt needs to be refinanced at much higher interest rates.

Debt default -> leads to depression -> crash in asset prices, particularly real estate

Home price / income ratios higher than they were in 2008.

What would the condition of bank balance sheets be if home prices were allowed to collapse and home price / income ratios went back down?

Greenspud: One of the other ways out of this, correcting the home price / income ratios, is if incomes rise to improve the relative cost of homes. But, I'm not sure if we are going to see that happen. Still possible as a way out of this.

MP: We are going to have both conditions of inflation and deflation at different times. Right now we are fighting inflation -> which causes disinflation -> leads to deflation -> which leads to the central banks flooding the system with money, which will cause -> stagflation.

MP: Wall Street is composed mostly of salespeople, whose job is to gather assets. For the most part, what people want to do is gather assets, plug it into a model that mirrors the S&P 500 and hope they never hear from their client again. When the S&P 500 goes down, they say the same thing: You can't time the market, buy and hold a 60/40 portfolio is the only way to go.

I agree with Michael Pento on the sales objectives of the financial industry. I noticed this a long time ago as a kid in high school that financial advisors seem to recite the same statistics about the S&P 500 and market timing and repeat the same "buy and hold" dogma. It's very cult like without any room for independent thought.

After seeing so many people close to me get devastated by the 2001 and then the 2008 stock market declines, I decided that I want to be more active in my investment decision making. It's my quest to figure out this game so that if I lose money, it will be by my own decisions and not of some financial advisor whose sales objectives are misaligned with my objective.

You're either an asset gatherer (a sales person) or a market strategist who studies the market and let your track record gather the assets for you.

We've had the longest inversion of the yield curve in 43 years.

Leading economic indicators pointing to recession.

34:00 Credit spreads remain quiescent. 4% on the spread between high yield and Treasuries.

Labor market - companies announcing layoffs 200% of last year. Nonfarm payroll report, index of aggregate hours worked, shows lower number of hours worked in October vs January.

You can double the number of jobs, but income and hours may not be there. (quality of jobs is worse despite number being the same)

Household survey shows October decline of 348k jobs. Household survey usually leads the establishment survey.

Fiscal drag - there's no real fiscal boost coming. Pandemic related savings will continue to erode in both nominal and real terms. Inflation will lower the standard of living. Groceries are up 25% since the start of Covid. Incomes not up 25%.

The Covid mortgage forbearance programs (FHA and reverse mortgages) ending on November 30 of 2023. These people have not made a mortgage payment in 3 years. 70% of all mortgages are FHA insured.

Student loan payment resumes supposedly began on September 1. Biden had an on-ramping clause that credit score will not be affected by not repaying the student loans. So MP is dubious on the impact of student loan repayments.

The employee retention credit - tax credit of up to $28 per employee - expired on September 14.

Conclusion - we are starting to see the "lag effect" taking place now.

40:00 Black Friday sales - higher end consumers getting frugal

MP: Corporate bankruptcies up 40% last year.

Expecting by the end of the first quarter of next year - market starts to break, needing Fed intervention. Sees only a "small chance" Fed lets BTFP expire.

41:47 Reverse repo facility running out - going to basically $0 - this facility usually has $200B (did he mean to say $2 trillion?) in it, we are at $800B. Trajectory should be $200B or less by March of 2024. At that point there's chaos in the bond market.

I'm unclear what he means by the reverse repo facility "running out"? Is he saying that they don't have enough cash to buy back the collateral? It's unclear to me what it would look like if this program "runs out". This video might give some explanation for what he's talking about:

MP: Has been holding short duration bonds for most of 2023.

Believes there will be a very narrow window to invest in $TLT and zero-coupon bonds, followed by

Deficits usually rise 200% in a recession. Our deficit could easily be "$5-$6 trillion after the next recession occurs". If the Fed buys all the debt, we will see stagflation. If they don't buy the debt, interest rates will go into the double digits. On top of massive bubbles in real estate and stocks is untenable.

There is no way you can have a viable economy with that much debt and that much asset bubbles and have interest rates go to double digits.

Automatic stabilizers will kick in - like food stamps and welfare. In the 2008 financial crisis, deficits went up 200% and it could happen again.

45:00 AT: How are you positioned now? And how do you plan to shift your current positioning if the things you think will happen happen?

MP: 70% of the portfolio in short duration Treasuries. 7-8% position in gold. 7-8% position in defense stocks. Long the dollar (have been long the dollar for 2 years, was a 10% position and down to 3%). 2% short junk bonds, going to take much higher. Anti-beta play - an ETF that shorts the higher volatility stocks and long the low volatility stocks of each sector.

When MP's model tells him to, will take the short duration bills and leapfrog into 5-7 yield treasuries. (i.e. $TLT-like position) because of flight to safety. The short duration T-bills won't be yielding at that time because the Fed will be in a rate cut cycle.

When economy starts to get stimulated again, that will be a big risk for long duration Treasuries because they get hurt by inflation.

Fed will be forced with a choice:

Let the gravity of the situation wipe out asset prices

Print money and have inflation, low real returns and low nominal interest rates. Gold rips higher.

Inflation erodes the middle class.

I remember hearing many of these same arguments around 2008 when the government was responding to the financial crisis and coming up with QE. I was just hearing it from a different group of folks - I think Bill Gross's newsletter had similar themes if I recall. But there were many opinions like this back then. Was the outcome really as bad as they said? Well... the talk of low real returns and stagflation at that time was enough to scare me out of investing in the stock market when it was actually a great time to invest!

51:00 AT: Bond trade safety trade. The idea that bonds will go up when the Fed responds by buying them again. Will bonds go up?

MP: Initially, you could have some flight to safety. Backtesting, back to 1981, 1987, etc... one problem they had was not enough inflation. I don't quite follow what he's saying here.

Believes the time period to be long bonds will be a shorter window because supply has never been this high and they know we are headed to inflation. Would be cautious holding zero coupon bonds and $TLT. It will last for a few months, but not for very long.

54:18 AT: When the market wakes up to this and we get the 33% decline in the S&P, during that period, MP has previously alluded to 4 horsemen - T-bills, US dollar, physical gold, short positions.

S&P 500 is trading at 18.5X forward earnings. That's assuming an 11% surge in earnings. The historical 10 year average is 17.6X. S&P500 dividend yield is 400bp lower than the risk free rate. Total market cap of equities right now as a percent of GDP is 116%, higher than any period prior to the outbreak of Covid.

We have a bear market started in the end of 2021. Brief reprieve in 2023 in a few stocks. Phase 2 is happening in 2024. Level that S&P has to fall from is higher than any other time prior. So watch out below.

My final thoughts on this interview is that Michael Pento is an active manager, so he's closely watching market conditions and adapting his immediate actions as he sees fit. His timing could be wrong again in which case he would adjust his plan. But, you or me we don't have the same thought process that he does so it would be hard for someone else to play Michael Pento's strategy unless you were to hear his updated opinion on a daily basis.

I think this interview cites many pertinent facts and possibilities to look out for. However, it probably won't play out exactly in the same way stated here. Things could get really bad if there is some kind of monetary crisis, but there will also be opportunities. Use your own strategy for when that time comes.