Adam Taggart / Darius Dale Interview Notes 8/11/23

08/11/2024

Assessment of the global economy and financial markets:

Economy and asset markets are at a crossroads:

Economy has grown uninterrupted since 2022. We are cresting off the top off that growth and now looking down the hill.

Asset markets - 42Macro models see debate between "goldilocks" regime (rewards for risk on) and "deflation" regime (flight to safety, bonds). ~4-6 weeks ago.

Overview of the 42 Macro process

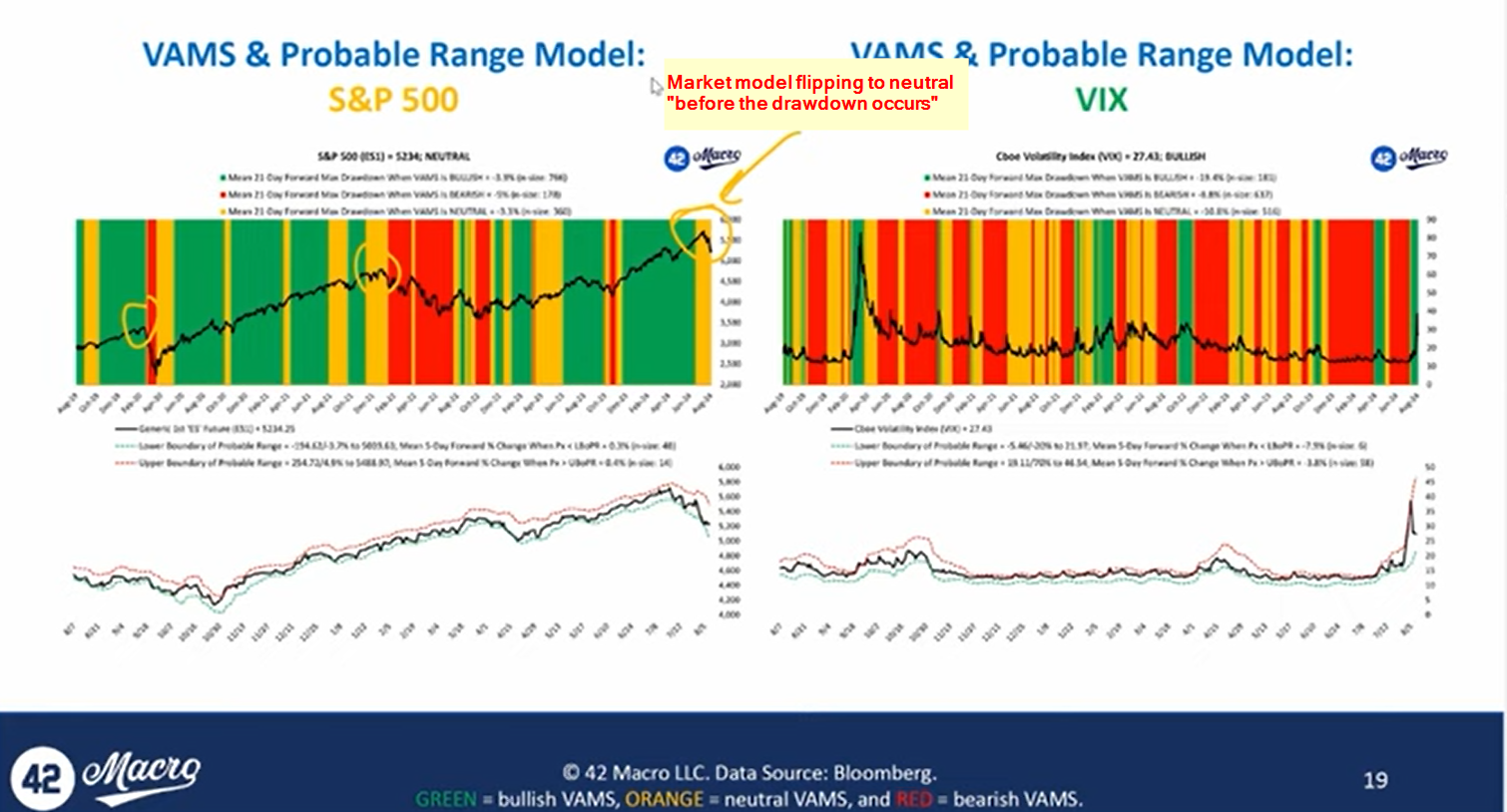

12:22 Are we in deflation now or is it coming?

This is concurrent. Happening now. For example, 10Y has been bearish going back to July. Volatility of that asset is confirming negative price movement.

Only ~3 times per year when the transitions matter. Trying to identify when the regimes change so investors can position.

We've been in a risk on regime since November of 2023.

16:00 Early 2024 interview he was very bullish. Are you no longer so bullish?

Cautiously optimistic. Not a high risk of a US recession medium term (3-12 months)

Q3:2024 - models slowing growth, deflation. Possible inflation in early 2025.

Historically 14% of megacap growth has come in deflation environment. So some equities can still rise even in a deflationary environment.

For this environment, favors: megacap growth, quality, large caps, dividend compounders, consumer staples, healthcare, utilities, information technology.

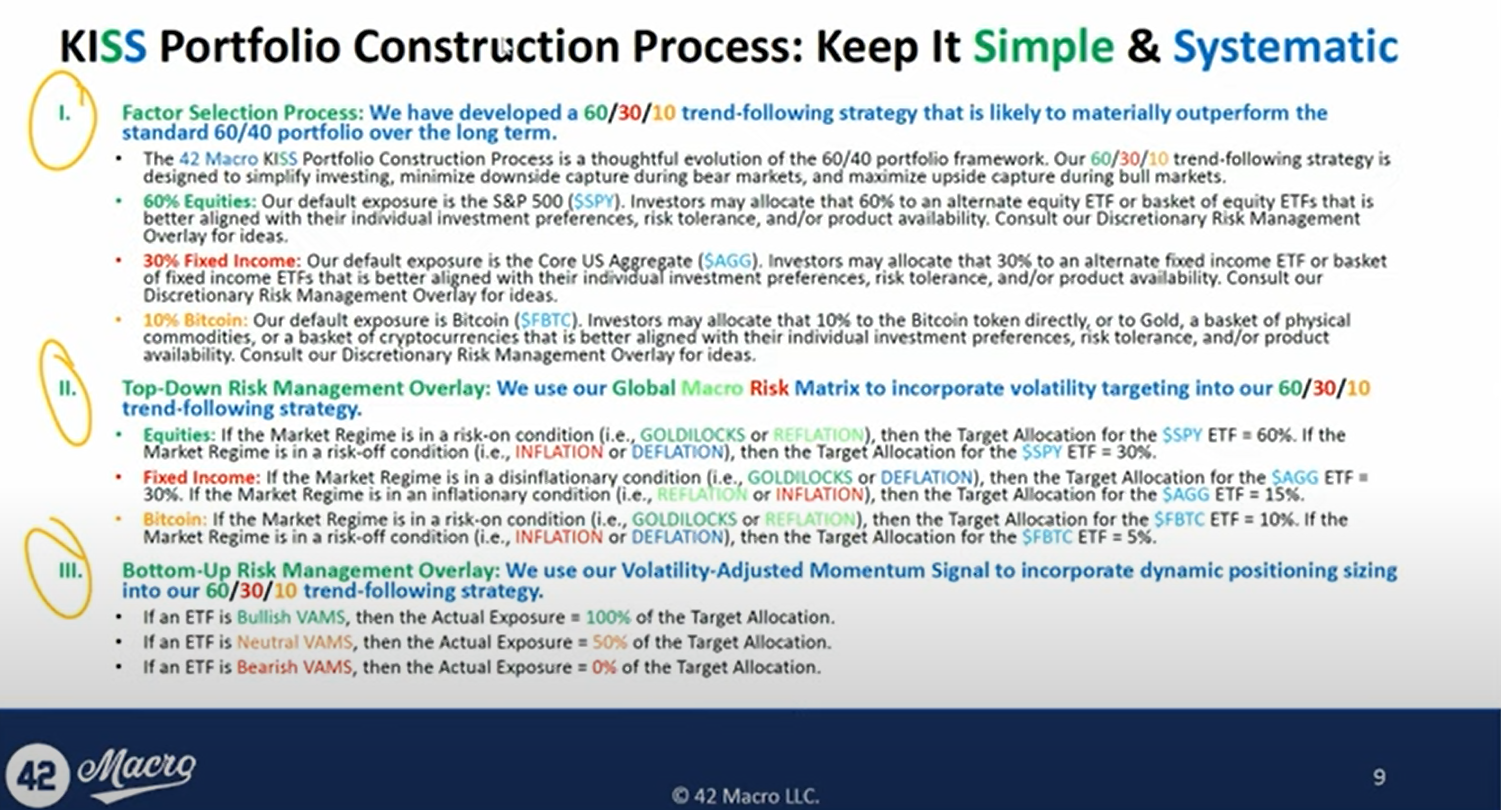

3 elements of portfolio construction method (KISS)

29:00

Will tell clients to get back in after a crash or significant correction. A lot of what I hear out there is "bear porn" which "gets myself paid but not my client paid". Greenspud: LOL

Went to 0% in Bitcoin allocation. Bought back into it 5% of portfolio position for the recovery.

KISS method - easy to execute. Only ever 4 ETFs in the program and 4 trades per month. "Keep it Simple and Systematic".

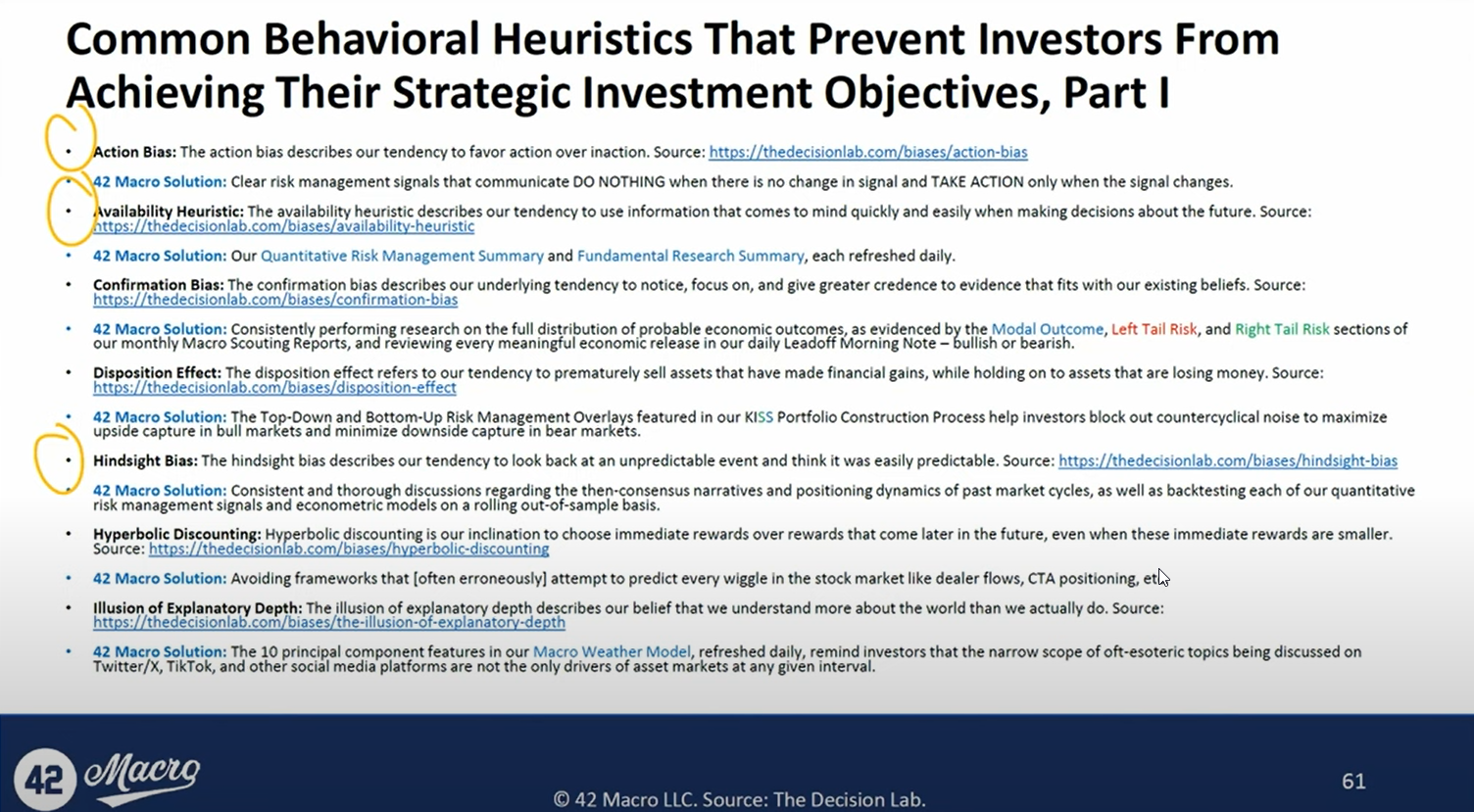

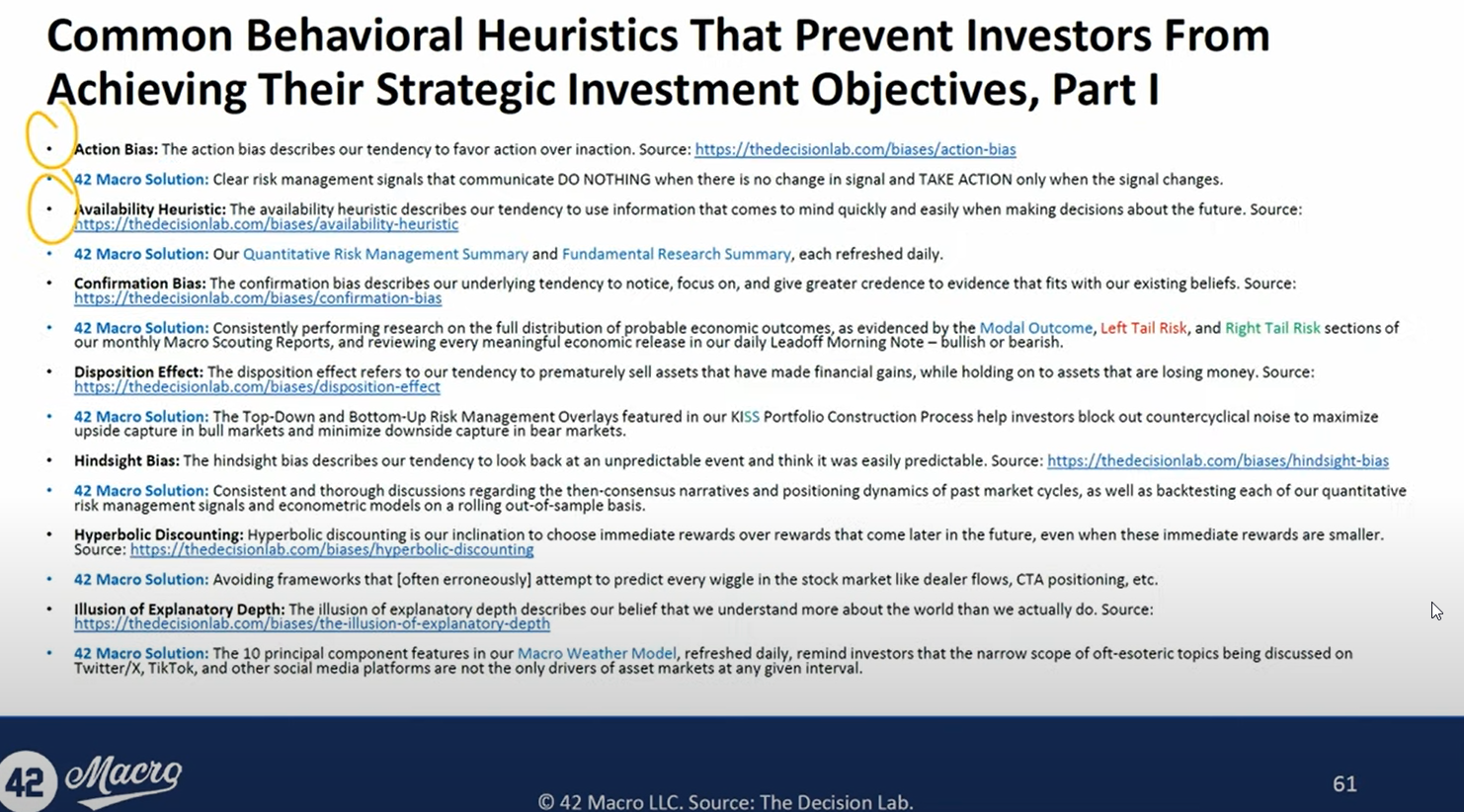

33:00 Helping retail investors overcome biases that sabotage returns

35:00 42Macro is looking into creating an ETF based on KISS

43:00 Statstically we hit the bottom of the cycle and recover - as long as we don't have a recession.

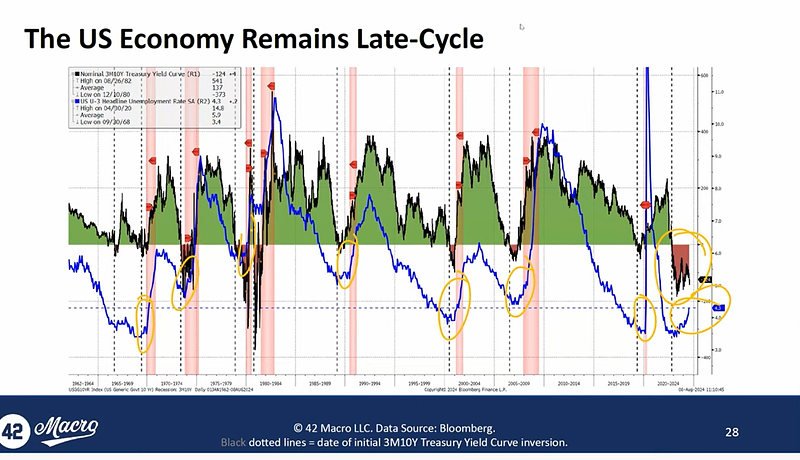

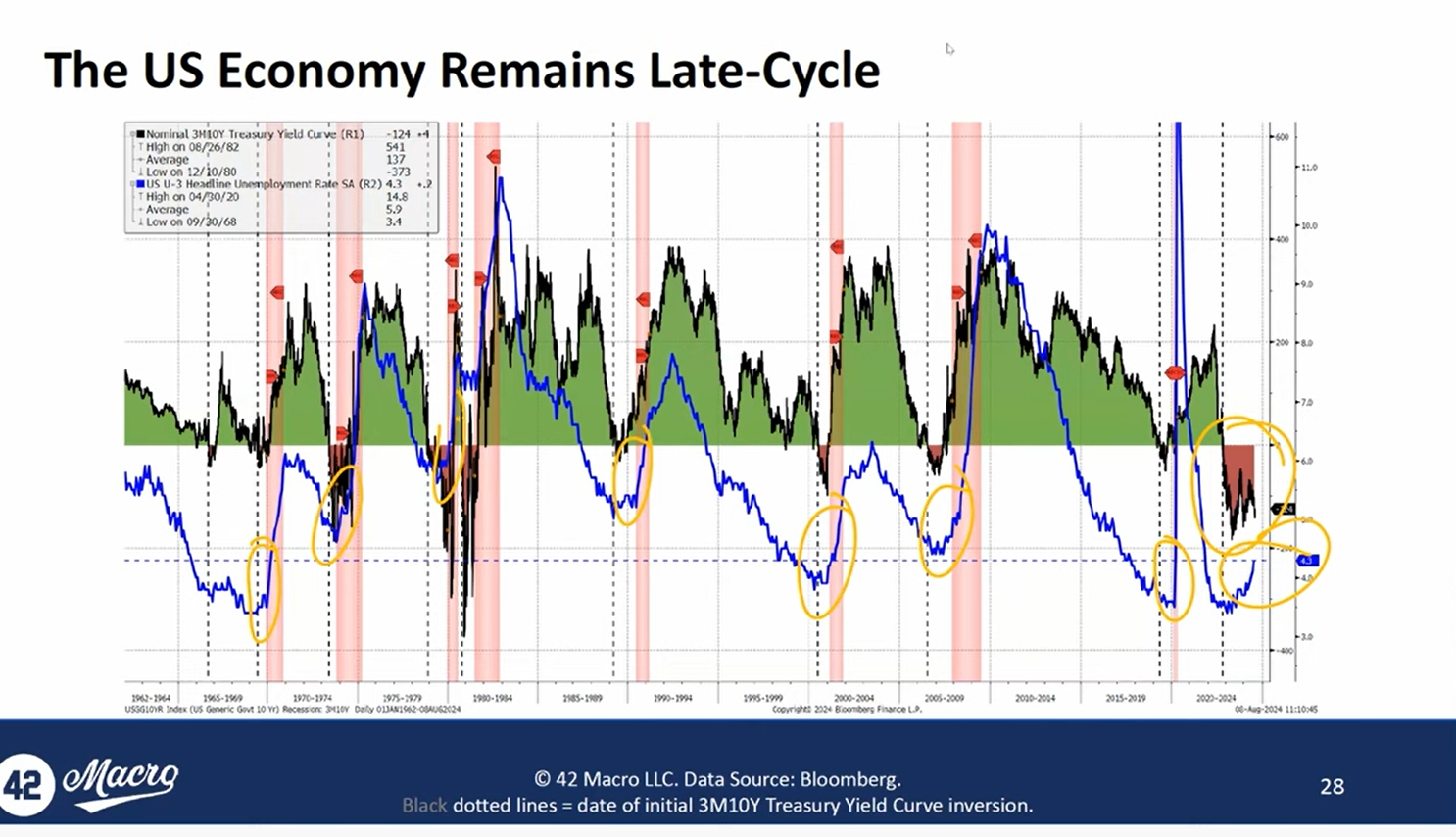

How has the economy evolved around recession?

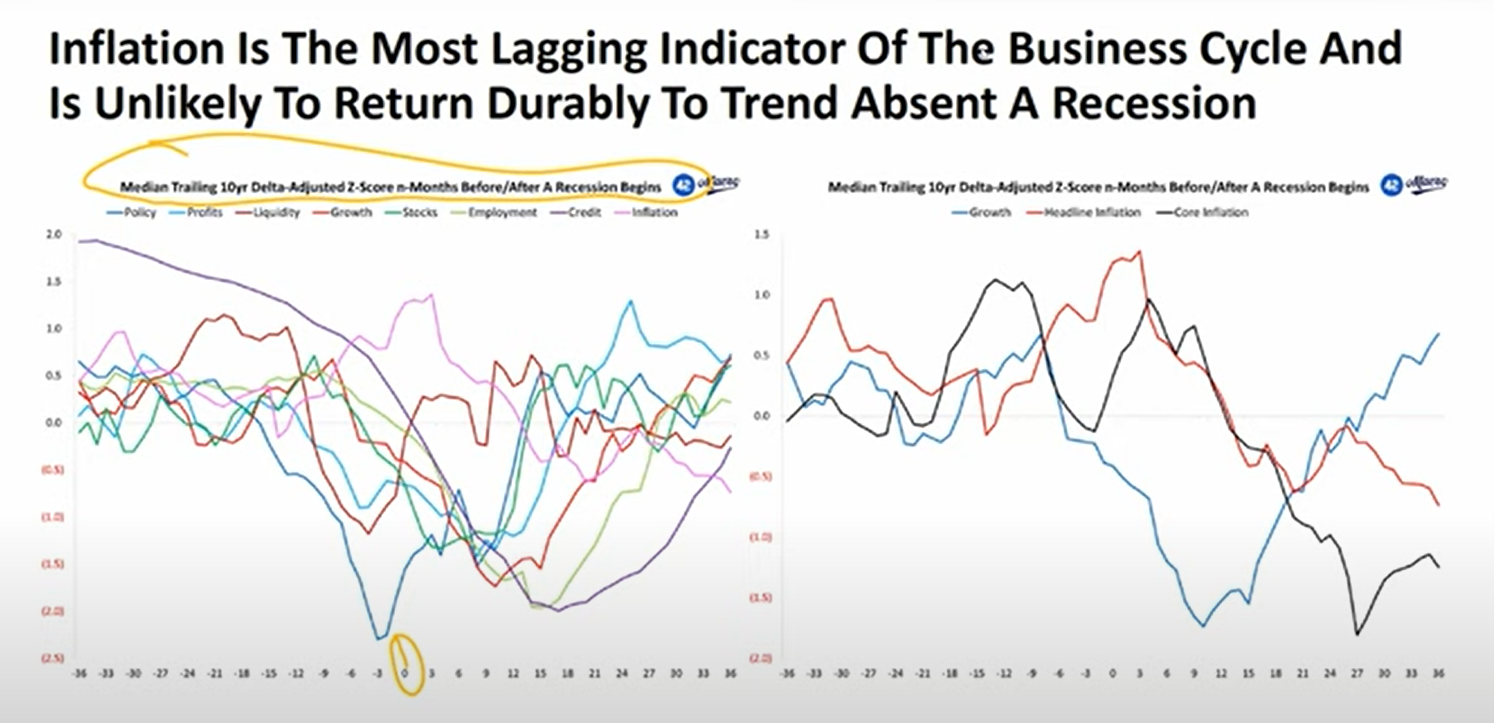

Inflation is the most lagging indicator of the business cycle. When heading into a downturn or slowdown in growth, How that typically works is in this order: policy tightens first, corporate profits break down, liquidity breakdown, growth breakdown, stocks breakdown, employment breakdown, credit breaks down, 12-15 months after recession starts inflation breaks down below trend. This was one of Darius's big "aha" moments.

Does not see performance of these metrics aligning for recession right now. Monetary policy is tight, but we don't have the other breakdowns in alignment.

Anything can still happen, so he needs to constantly update and monitor these models.

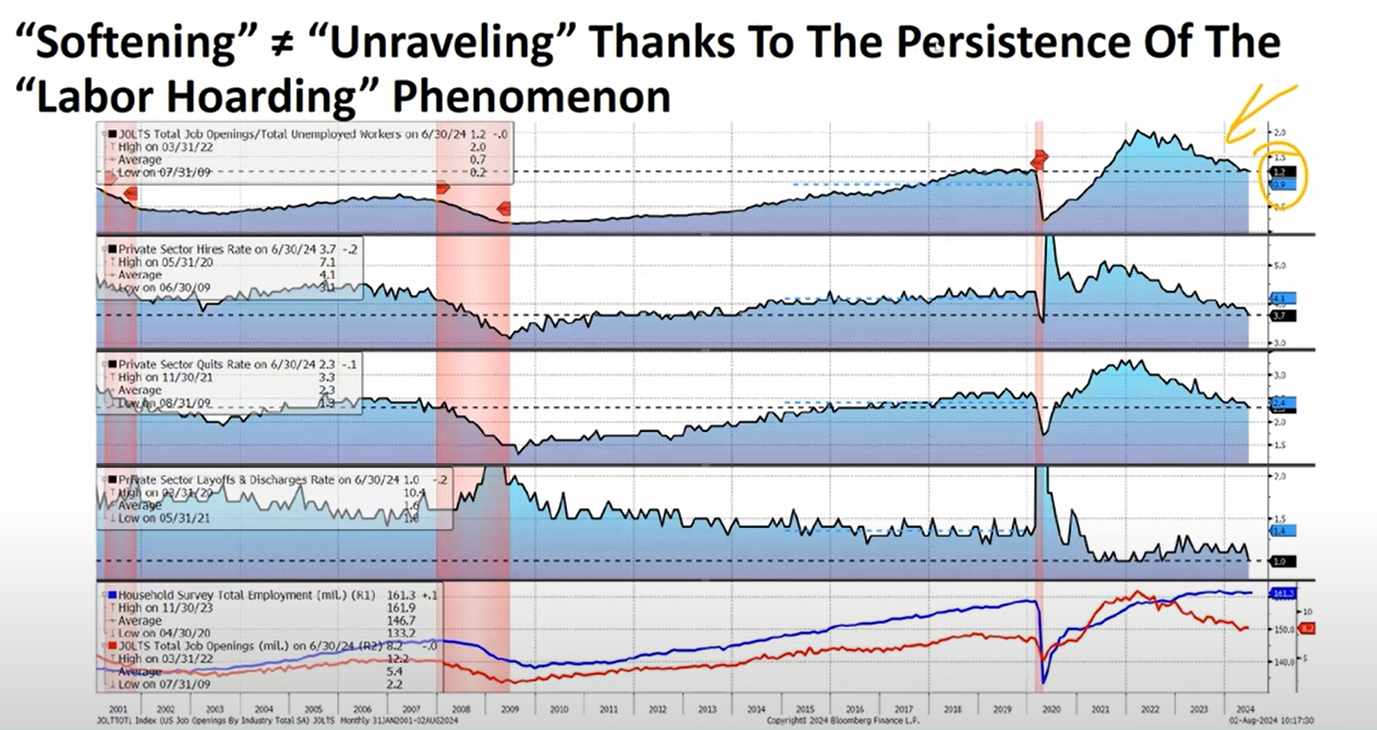

51:00 Adam asks about the significance of unemployment rate (basically asks about the Sahm Rule trigger without saying "Sahm Rule")

In July when the Sahm Rule was triggered, we had a 425k+ addition to the labor force from migrants.

"Labor Hoarding" - some indications of slack being created in the labor market but not deterioration of the labor market, which is unusual historically speaking. (i.e. not a lot of firing going on)

Since 2022 - divergencs between JOLTs total job openings (declining) and household survey total employment (growing). Unusual because we've previously always seen a positive correlation between the two. Never seen "labor hoarding" before. So there is a softening in the labor market, but we are not seeing deterioration.

1:03:00 Investing for the 4th turning.

A crisis is coming and we need to be prepared.

Risk of a US fiscal crisis is much sooner than the average investor realizes. This decade

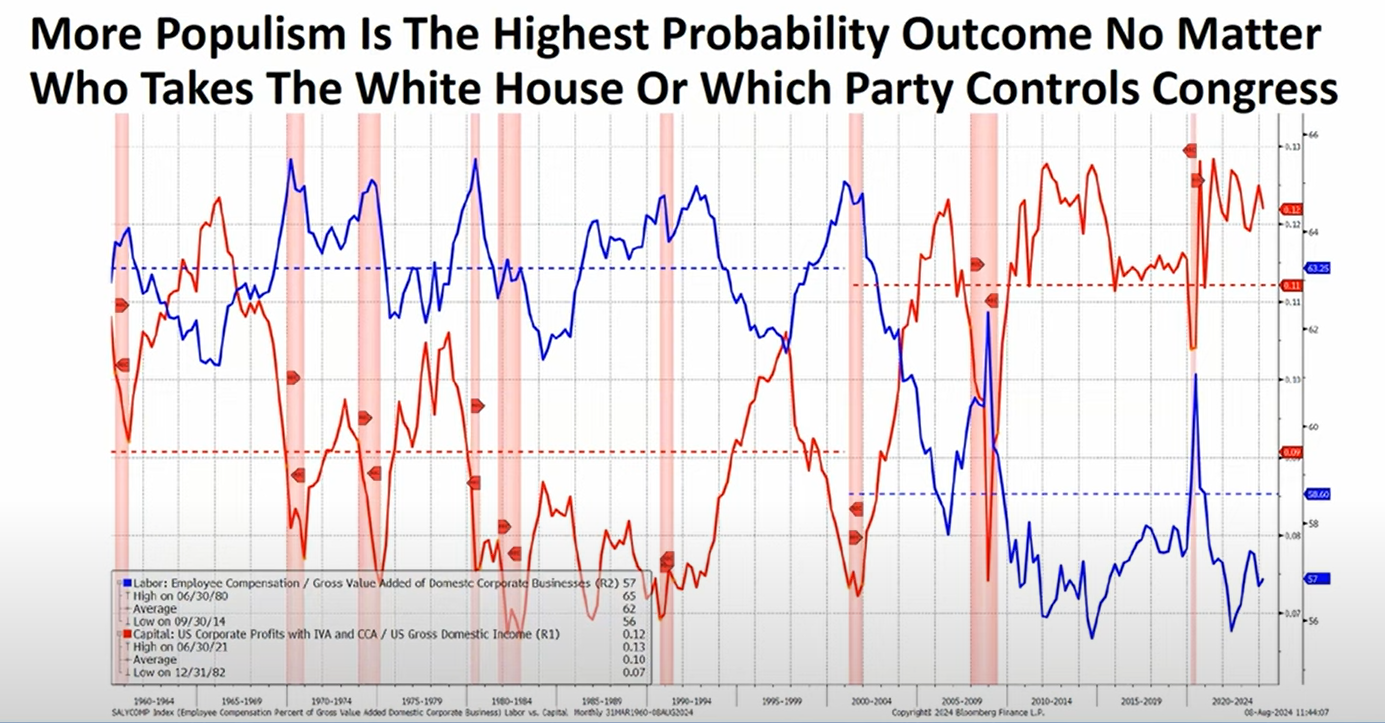

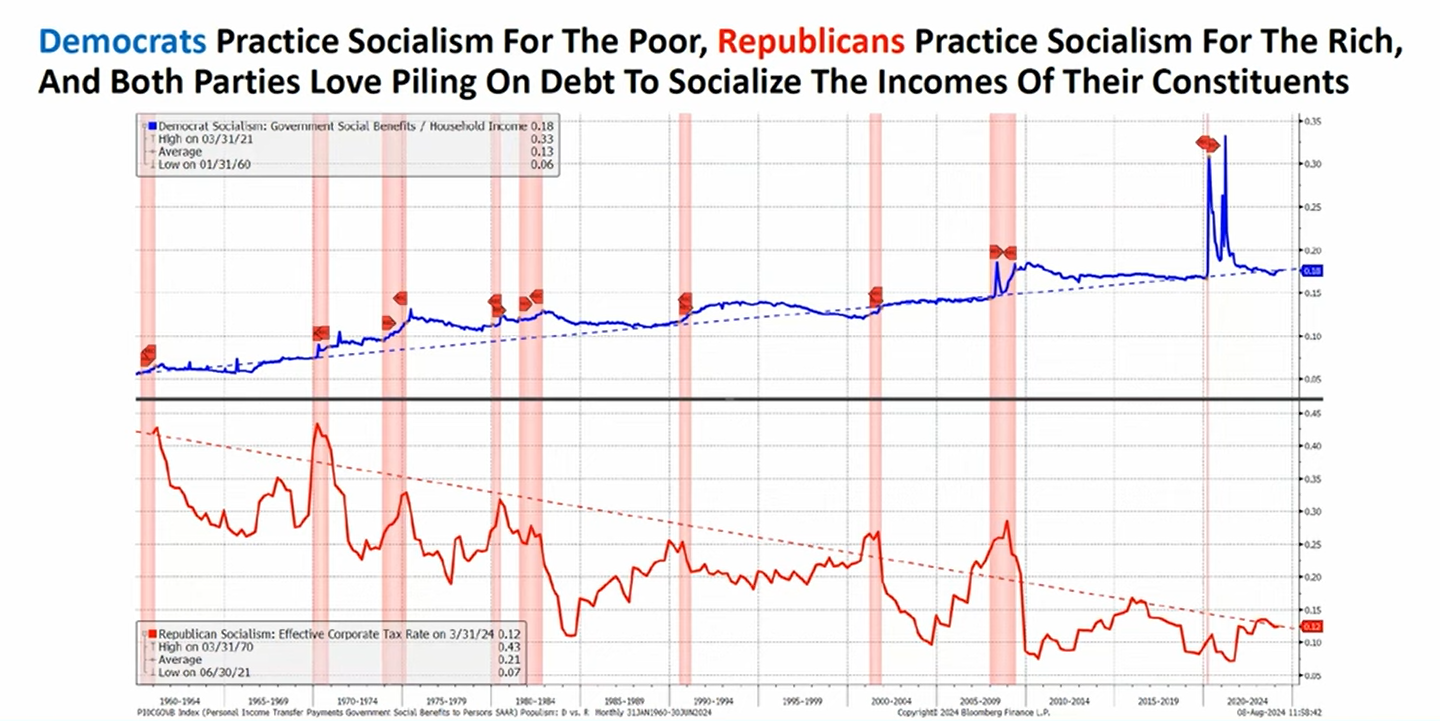

Socialism requires debt! Blue line in chart is rise in government benefits vs household income. Red line is corporate tax rate. Democrats overspend, Republicans under-tax.

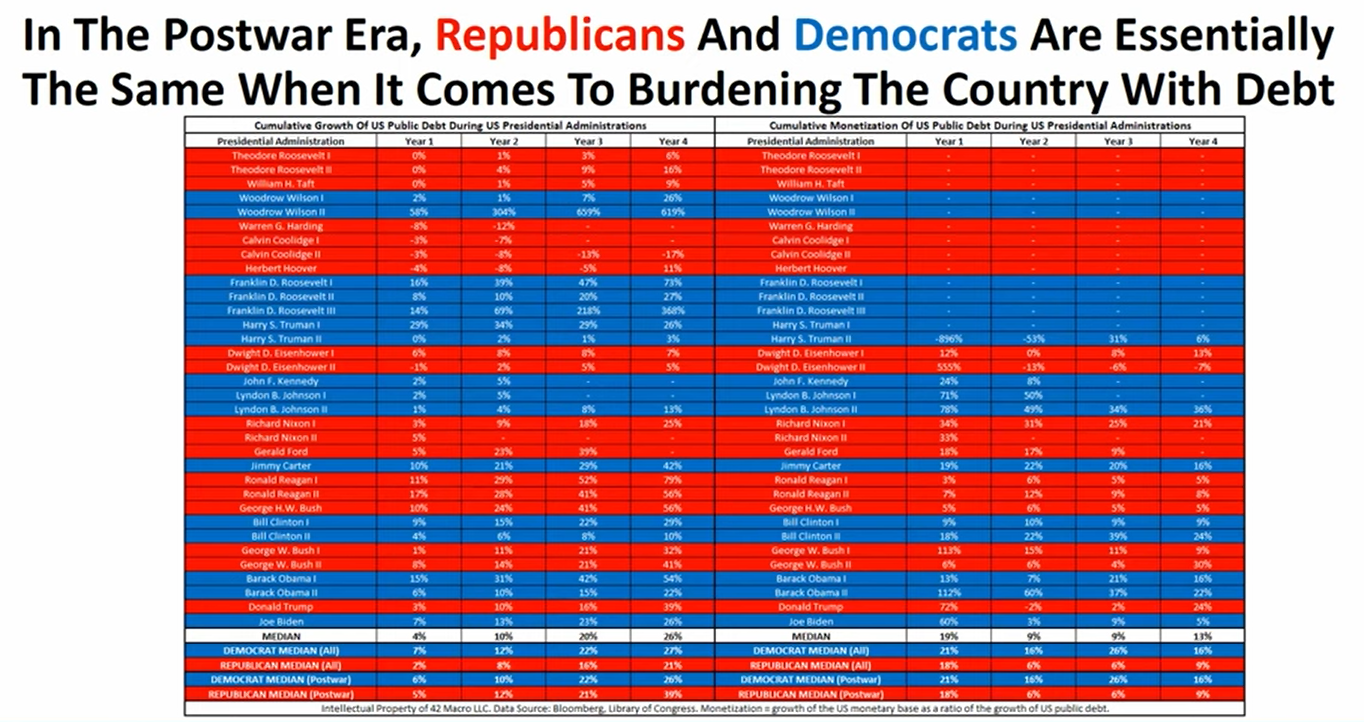

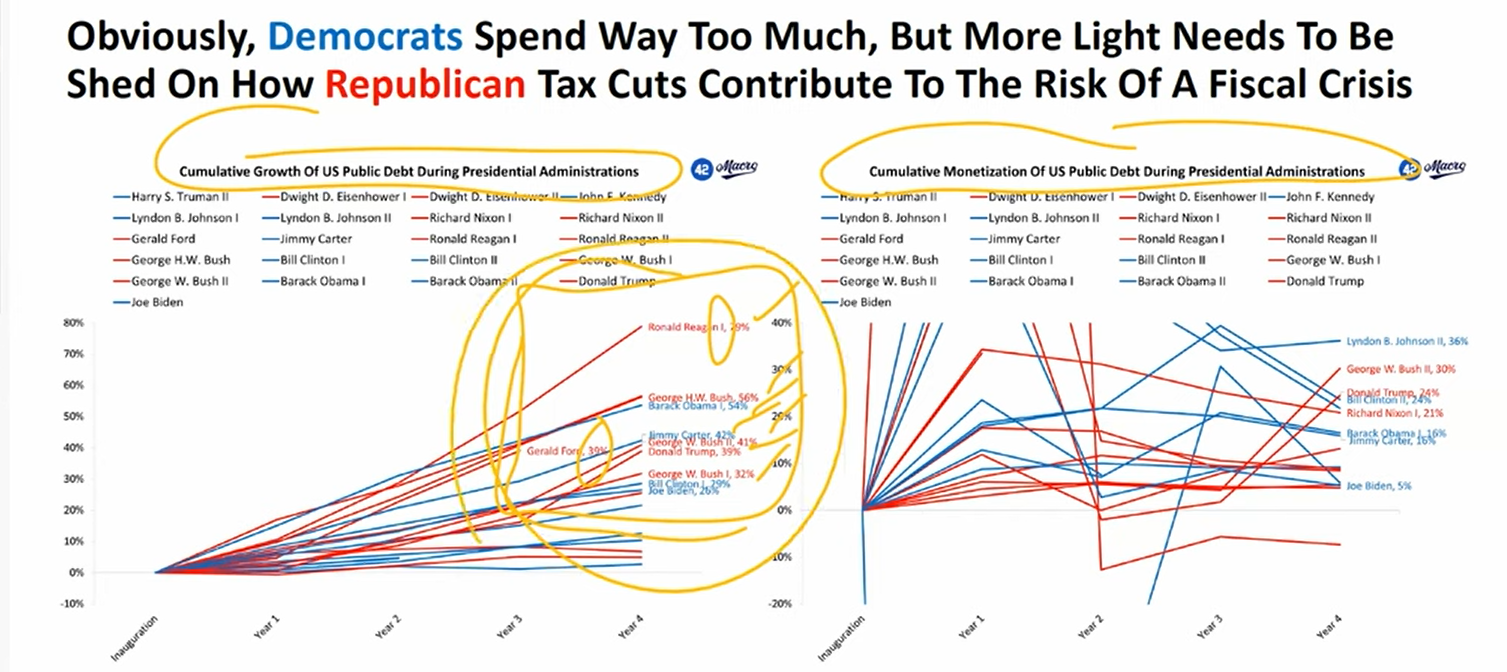

In the postwar era, both parties are the same when burdening the country with debt.

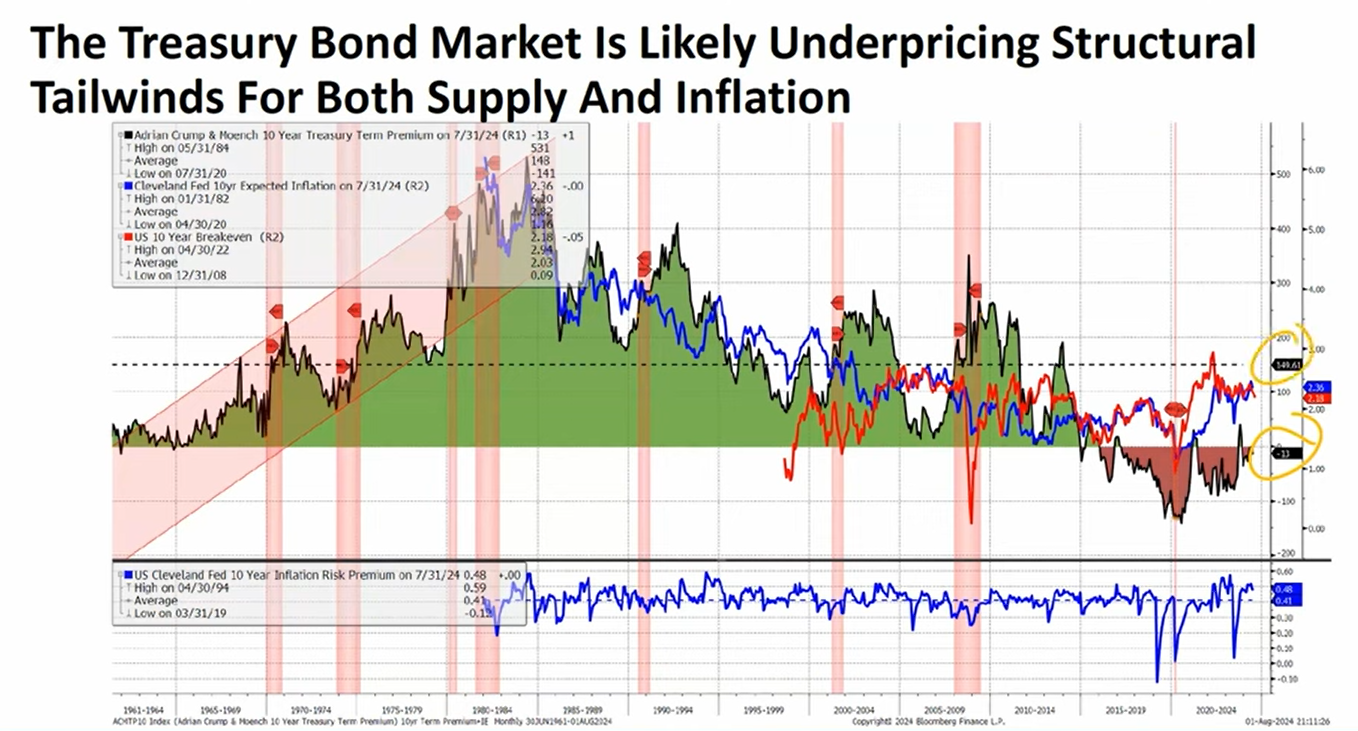

Term premium in the bond market - 10Y is underpriced. Historically has averaged 150bp of risk premium.

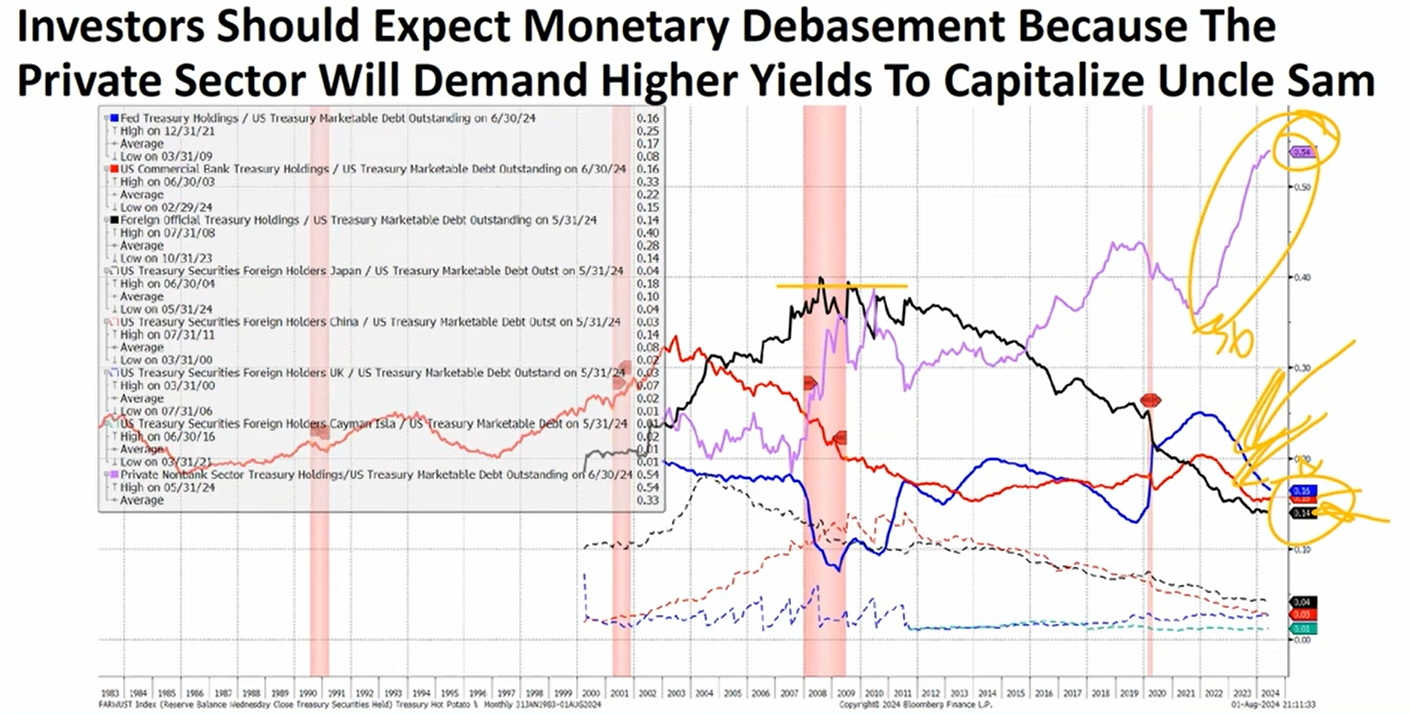

This chart shows that the private nonbank sector is the biggest holder of treasuries, thereby with the most risk exposure.

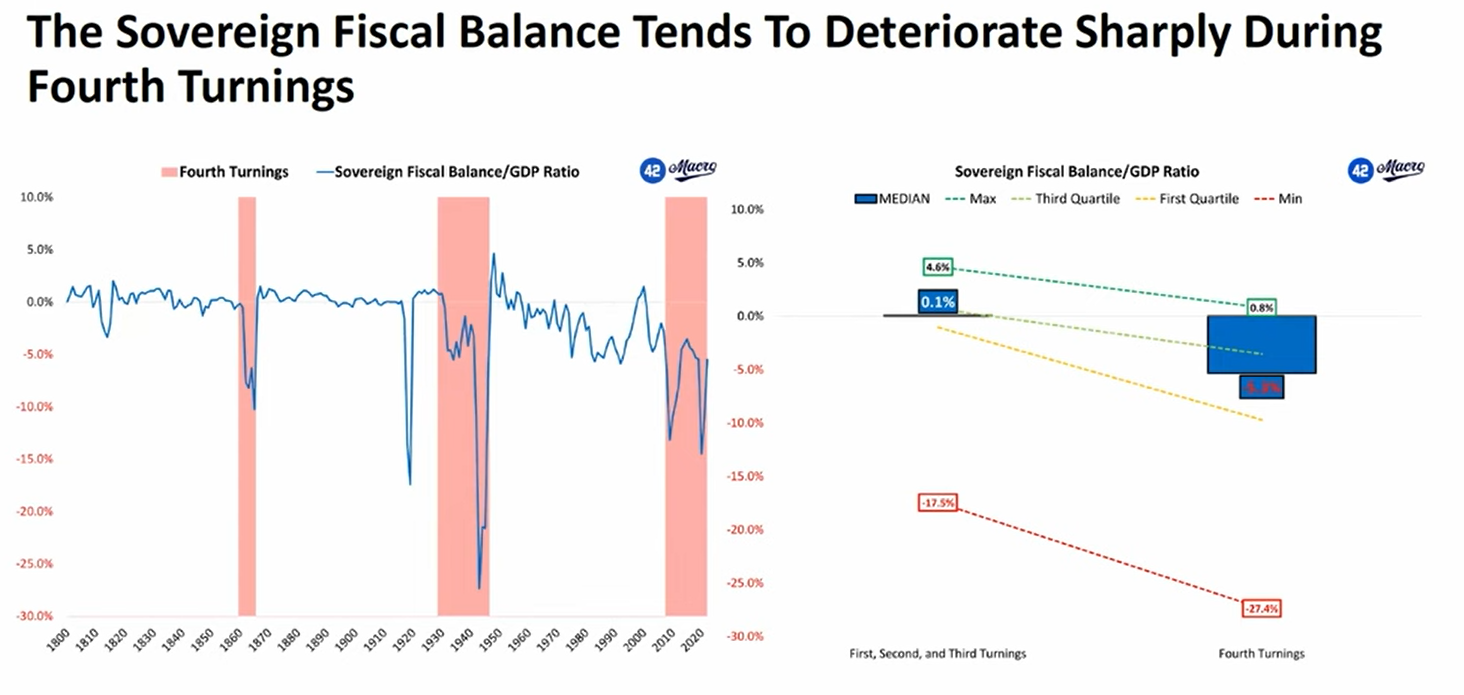

Budget deficit always widens in a Fourth Turning. We know that the public sector balance sheet is weaponized to fend off a crisis. We haven't even gotten to the fiscal crisis yet.

Greenspud: This last section of Darius's lecture on the fiscal irresponsibility was quite a change in tone from the previous interview he did at the beginning of the year. In that interview he had an agnostic viewpoint on public policy, saying that it doesn't matter, his main goal is to make money from it. This time he actually expressed concern about the potential crisis coming caused by reckless government spending.