Reviewing the Reverse Repo Interview - Adam Taggart / Lance Roberts Interview Notes 4/8/23

12/27/2023

1:00 Adam is having difficulty replicating his backdrop for the new studio. (And probably at this time did not expect it would become obsolete not long after when he leaves to start his own company! 😆)

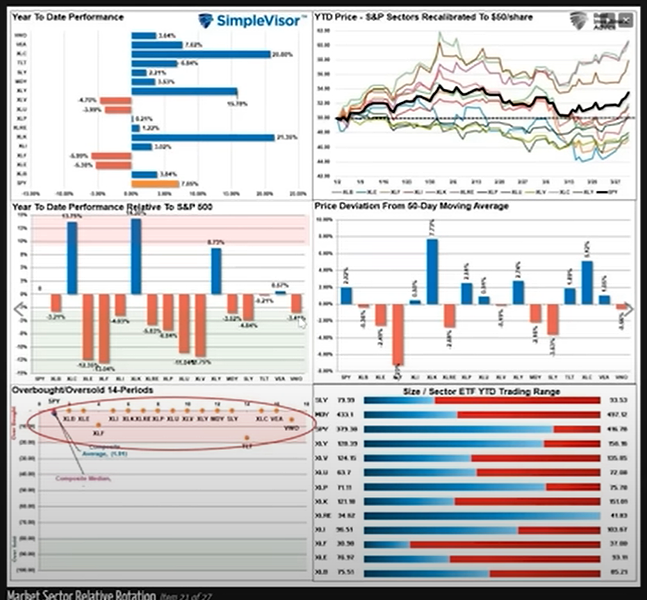

3;00 Narrow rally, 88% of the gains coming from the top 10 stocks

Market taking off after jobless claims data

Rising bull market vs

Lower left chart - every sector seems overbought -> possible correction.

Tech, consumer discretionary performing well. Energy underperforming.

A lot of the reason for the concentration in the top 10 stocks is the concentration of a few stocks in all the ETFs. For example, $AAPL is in 87 ETFs.

The rotation is that money is coming out of energy.

Deviation above and below the long term moving averages.

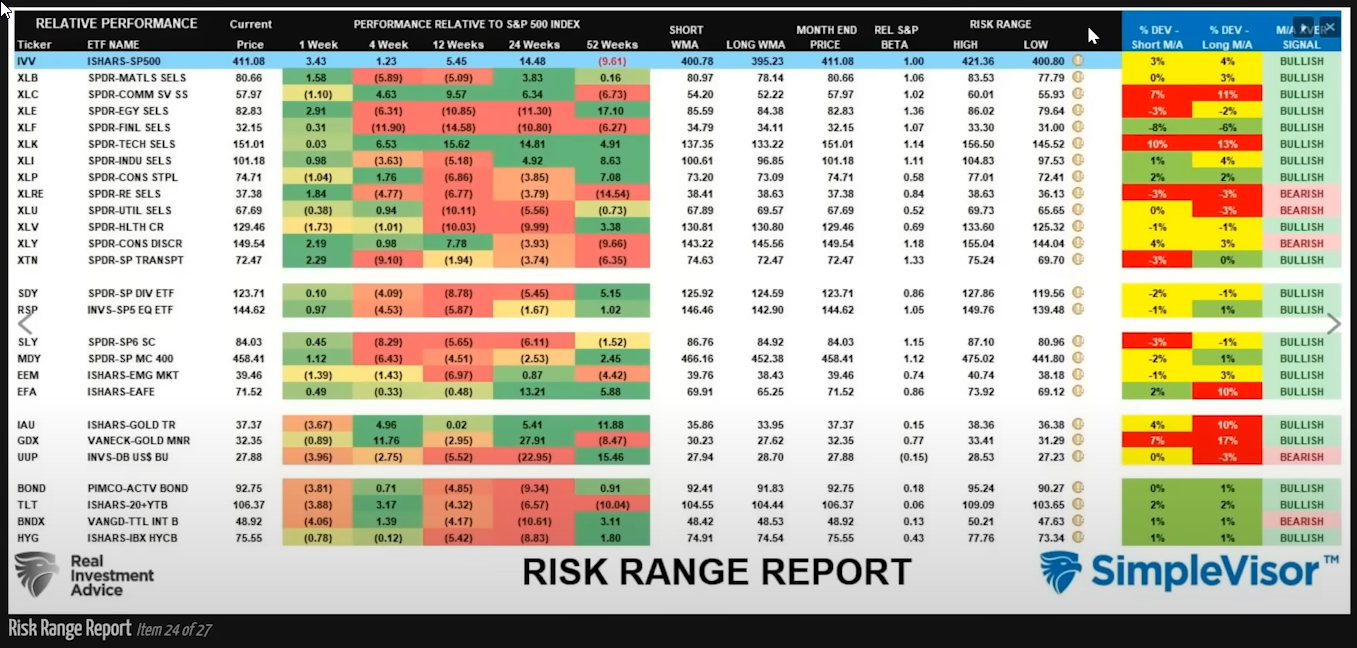

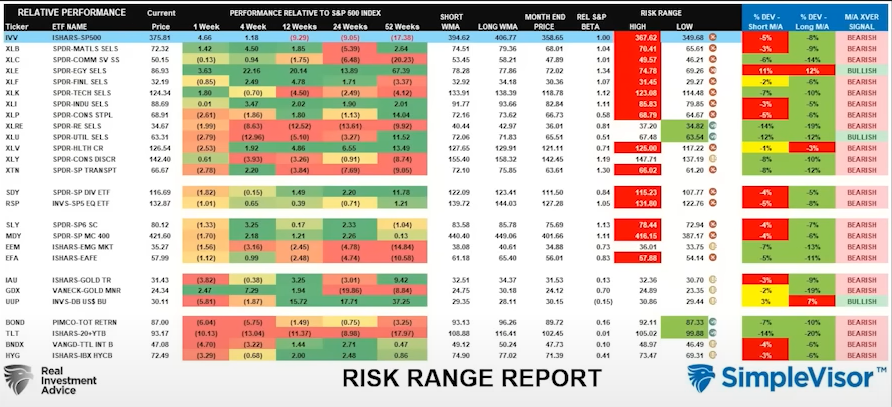

Vast majority of markets are in bullish trends.

October 2022 showed every sector an market in bearish territory. Only real estate and utilities were trading within their risk range. Now those two are showing bearish.

17:00 Reverse repo market problems

It's kinda like the de-dollarization debate. It's an issue, but not going to cause a problem in our lifetime.

Reverse repo is a program by the Federal Reserve. Anyone with access to the Fed window can take advantage of the program (money markets, investment banks, commercial banks.) They make an agreement to hold Treasuries overnight and sell it back to the Fed at a higher price (which is the interest).

The reverse repo rate is used to adjust the market to keep the short term interest rate within the Fed Funds target rate.

$2.5T is sitting in the reverse repo program. During the 2008 financial crisis it was a very small amount by comparison (like hundreds of millions). The reason it is so high now is because of all the excess liquidity pumped into the banking system from the 2020-2021 period.

This is putting stress on banks.

Lance talked about how banks aren't really paying customers interests. They are taking deposits and using the reverse repo facility to make money on the deposits and not passing that through to customers. The major brokers like Schwab are yielding 0% on accounts, Interactive Brokers was unusual by offering 4%.

Banks don't want your deposits because right now they don't have a good place to lend. Delinquency rates on credit cards and auto loans going up. Lending standards are going up.

Banks don't want to lend out the money because consumer loans are risky. Where else can they put the money?

Banks also need the collateral. SVB (Silicon Valley Bank) got crushed because the value of their collateral (long term Treasuries) declined when interest rates went up and that's what crushed them. SVB was buying "safe" assets, but the duration burned them.

Adam: Why wouldn't banks do this? Talking to Nick Gerli - because rentals are not as profitable as they used to (i.e. capex rates not so good), why not just buy bonds from the Fed?

Adam: banks are getting free money from the Fed and are not sharing it with their depositors.

Lance: The banks have a problem, especially the regional and small banks. They make money by loaning out their deposits. Because the deposits can be called at any time, they need to invest the money in liquid collateral.

Bank balance sheets have two "pots" of asset securities as collateral: "hold to maturity" (usually a small sliver), the majority are "auctionable securities" (securities that are liquid).

Whats happened is that the "hold to maturity" pot grew as interest rates went up because they started classifying more of their collateral as "hold to maturity" to avoid taking an impairment. The liquid portion of their collateral has shrunk, making them even more risk averse.

The Fed could discourage use of the reverse repo facility by lowering the reverse repurchase award rate, making the facility less attractive. But, the Fed doesn't want that because a lower RRP rate would incentivize banks to lend out into the economy, which would create inflation and counteract the Fed's efforts to tightening monetary conditions.

30:00 Banks aren't really using the reverse repo facility because they are distressed. The fed has incentivized use of the reverse repo facility by giving away free money via the RRP award rate. That effectively cuts demand in the economy by choking off lending activity.

Use of the reverse repo facility is keeping money out of the economy.

Quantitative easing - in 2008 we did quite a bit of QE and didn't grow the money supply. Money supply grew in 2020-2021 because we sent checks directly to households. By comparison, QE is just an asset swap with banks.

Greenspud: So is the reverse repo facility effectively a form of quantitative tightening? Sounds like it to me.

Why does JP Morgan pay only 0.01% on a deposit? Because they really don't want your deposit because they have to do something with it and they currently have no good place to lend it out.

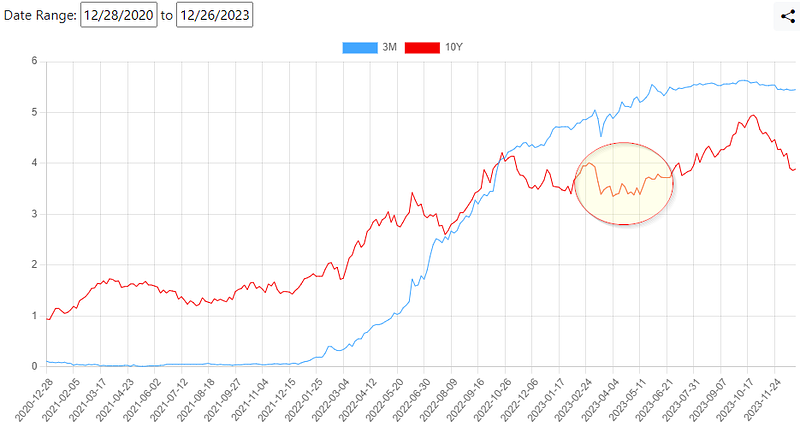

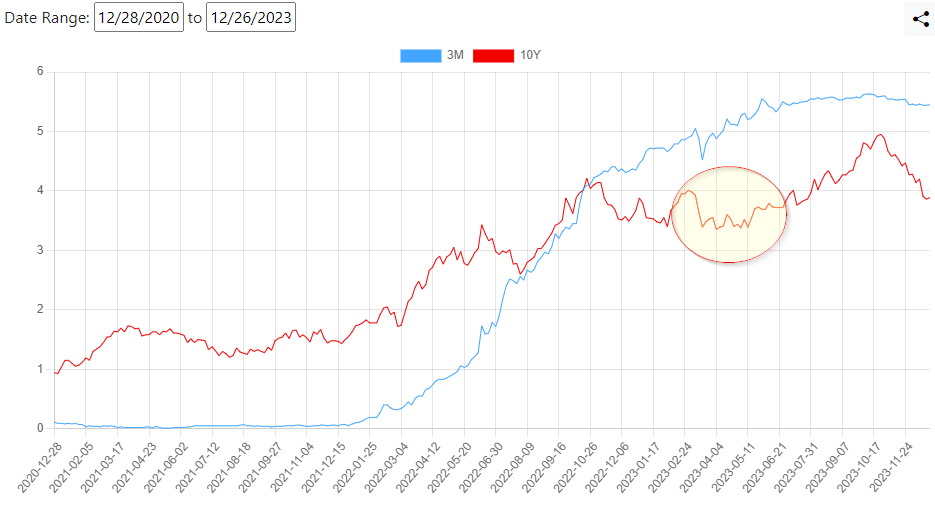

34:00 bond yields have been going down. Past week 10-year went from 3.2 to 3.1%. Over past month came down from 4.1%.

Failed technical breakout on the 10Y treasury. That's an indicator of weakness in the economy. Lance believed at this time that yields would continue to go down (he was wrong, they rallied to 5%).

Lance sees the declining yield on the 10-year as a recessionary indicator, a result of capital flight to safety.

Lance: "I don't know how we don't have a recession." ISM data, leading economic indicators, leading economic composite data - all points to recession. Fed hiking should cause a recession.

Services make up 80% of the economy, 20% is manufacturing. In the 70s that was flipped, which is why ISM isn't as impactful as it used to be.

This time is different because we've been training the markets to just respond to the Fed. Market no longer cares about the employment data - they just use that to interpret what the Fed is doing next.

Adam: read that there is still $1T in excess savings lying around from the 2020 stimulus.

44:00 Surprise oil production cut at OPEC - inflaitonary

Bank of Canada paused, Australia paused, India paused.

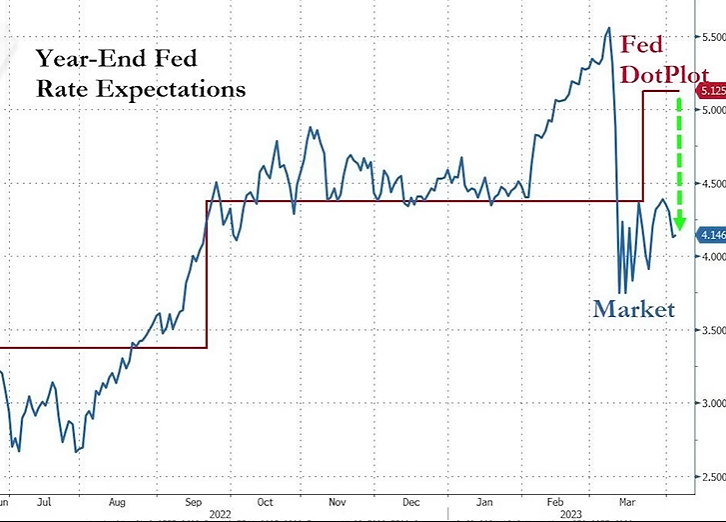

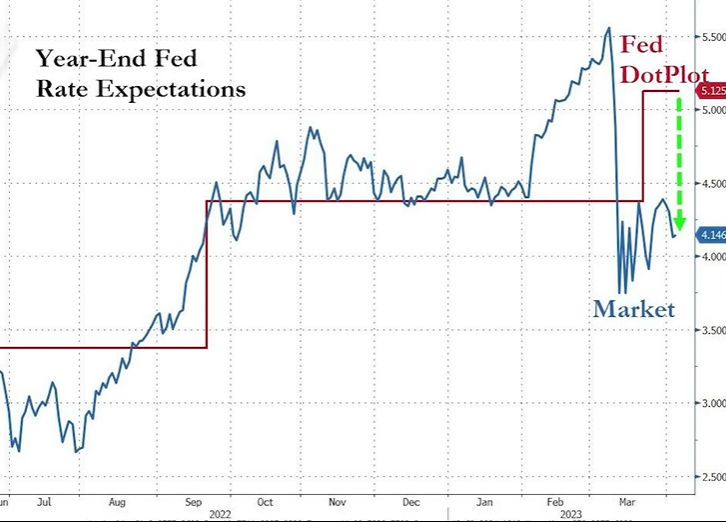

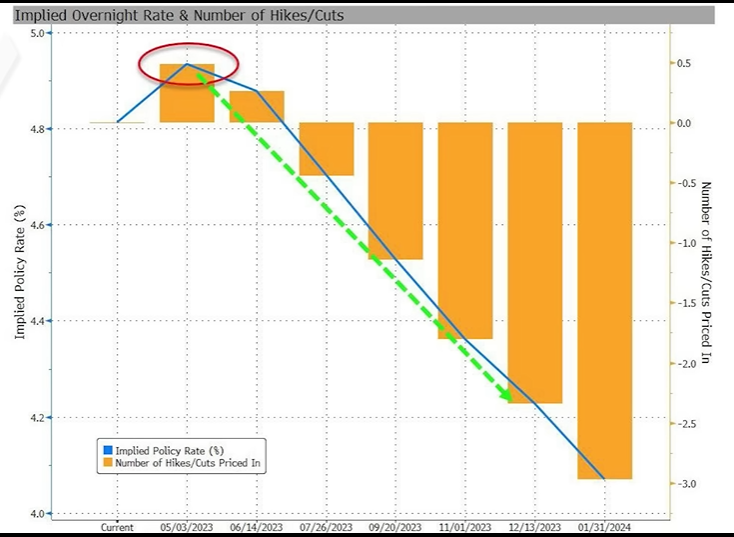

From Zerohedge, showing disconnect between market expectations and Fed dot plot:

Fed saying that even if they pause, they will stay for a while. No cuts anytime soon.

Market has a problem ahead. Earnings estimates high, and recently raised higher. Valuations too high for slower economic growth.

52:00 earnings beats are nonsense. They are usually beating on non-GAAP numbers, which excludes the "bad" stuff. If they used GAAP they wouldn't beat as often.

Public doesn't remember an analyst's downside revisions on EPS. Being a bull and an optimist carries more likability.

56:00 Gold - punched through $2000 level. Matthew Pipenburg - gold held purchasing power over time better than fiat currency. Good bet.

Lance: disagrees. Gold is extremely overbought. Correlation to the stock market is extremely high.

Long term gold has not held its purchasing power. S&P index has performed a lot better over time than gold. In theory it sounds great that it will hold its value relative to other assets. It's just a conversion of a store of value.

1:00:00 Ukraine

1:10:00 Revisions of government numbers - BLS uses crude estimates of sample data run through models to come up with the published unemployment numbers. Only about 20% of the reporting is based on actual data, about 80% of it is just estimates. We don't get accurate numbers until the revisions. A lot of the government numbers could be erroneous.

1:15:00 HOPE cycle - housing/orders/profits/employment. Will be interviewing Michael Kantowitz.

1:17:00 Layoffs. Tech sector 100k cuts this year. Highest pace since 2001. What's different this time is that we are beginning to see this spill out into other sectors of the economy. (Greenspud: really? no spillage so far employment remains strong it seems going into tne end of year)

1:18:00 Small businesses got devastated by 2020 shutdowns, but are now getting hurt by credit conditions. IRS wlil be raising corporate tax rates soon.

Have things gotten bad enough that things are starting to improve? Are we closer to the economic trough? Or are we on the cusp of things getting worse? We don't have the answer now.

Lance things the markets have not corrected enough. (wrong call in hindsight)