Adam Taggart / Danielle DiMartino Booth Interview Notes 12/07/23 - RRP Depletion and Creative Destruction

12/15/2023

2:00 current assessment of global economy and financial markets

DDB - Santa Claus rally came early. Markets usually get ahead of of itself when recession is coming.

In all 50 states + D.C. except for Texas, unemployment is rising according to BLS. In that situation, happened 9 times before. Each time had rising national unemployment rate and contraction in nonfarm payrolls in subsequent month. "Following those 50 months, the first, second, and in some instances third of those 9 episodes saw the S&P500 go up." Mindset has been there that since 1976 the Fed will come to the rescue.

It appears that the "biggest bond market rally since 1980" (i.e. this year's) pulled some of the Santa Claus rally into November.

In June 2022, QT started and has not stopped. Lag effect based on the current tightening will play out later. Final rate hike of June 2023 will also play out with a lag 12-18 months into the future.

"The Fed is pushing on a string". When Fed begins easing, they are easing against the effects of the lagged monetary policy. Doesn't matter when first rate cut comes, lag effect thwarts their efforts.

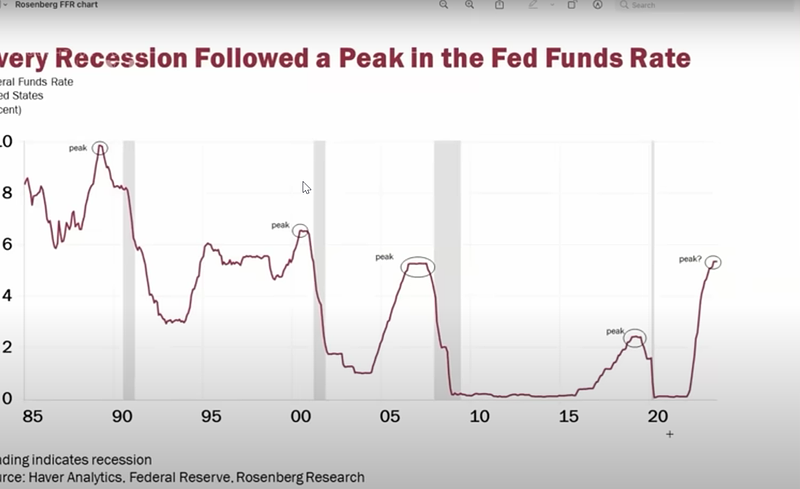

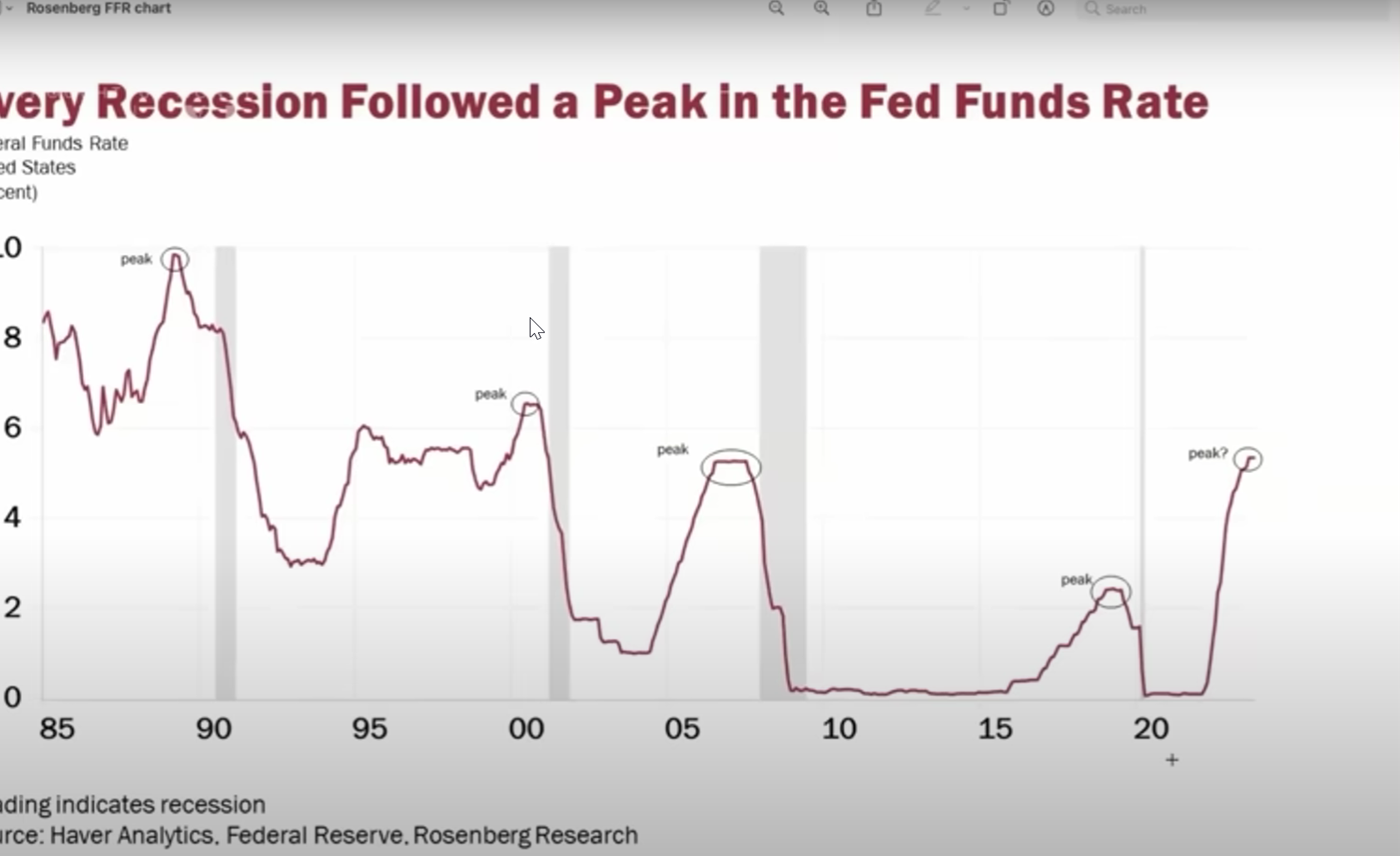

6:30 every previous Fed pause followed by a recession

DDB: Average lag effect is 7 months. Does not foresee the current Fed lowering rates by January 2024.

9:02 Should investors be reading for deflation next year?

DDB: Yes. How do you think markets would react if they saw CPI decreasing month/month? Last week France and Italy reported deflationary month/month (negative) prints. France is in recession.

Backlogs: ISM report fell to 39. In the 30s in most of Europe.

Germany looks like it will stay in recession in Q4 2023.

When disinflation turns into deflation, it creates an adverse feedback loop for credit conditions. For example, 23% growth in German insolvencies.

S&P just introduced Canadian PMI - currently "flagging" deflation.

12:00 AT: Collapse happens from outside-in. Weaker players fall first. The trajectory of other countries is into deflation/recession. Not just the smaller countries but the France and Germany now. Can it be a preview of what's to come?

DDB: disclaimer to suggest that Asia is "stabilizing". We need to be cognizant of its influence on the global economy. It's all relative. In our world, we tend to think it terms of dollar / Euro.

13:30 Asia not showing signs of strength. They won't be able to pull the global economy out of recession this time?

Moody's had a leak of info about downgrading sovereign debt of China. Had an immediate effect on copper.

~2015 there was a global recession similar to 2008-2009. China came to the rescue of South America and other exporting nations. Right now that's not happening, they are just trying to hold themselves together.

15:00 Fed - soft landing. What's more likely. Fed achieves its inflation target? Or will it be more along the path to that trying to happen, they break something?

Commercial real estate "WeWork effect: - acceleration of a typically slow moving victim of a credit crunch.

We thought banks had issues with unrealized losses on risk-free assets. What about their loan books? There's a lot of debt to be refinances in 2024. Companies have had the luxury of being able to refinance their debt. When companies get into the spring of 2025 - credit rating agencies can reclassify debt expiring within a 12 month window as a current liability. Acceleration of this will be real going into 2024.Greenspud: She's talking about the corporate debt maturity wall here.

19:00 Layoffs component of the coming debt maturity wall. This year companies have not been conducting layoffs at a big enough scale to matter. That may be coming?

There is a bizarre phenomenon now of companies buying back their debt on the open market and being labeled as defaulters.

Founder of DailyJobCuts.com is covering he whole country layoff press releases and local business closings. This month tallying business closings / layoffs coming seasonally early.

22:30 Bonds - may be sniffing something out. Looking like they won't have a third down year in a row. 23:30 Powell higher for longer - will he change that policy and cut sooner like Q2 2024?

DDB: believes there was an overreaction to Christopher Waller (Powell's chief lieutenant) signaling a third consecutive pause. Markets could be right about rates in March or May 2024, but Powell is still talking about QT - contracting the Fed's balance sheet. Powell: "Even if we lower the Federal Funds Rate, I want to continue pressing forward shrinking the Fed's balance sheet. It is the shrinking of the Fed's balance sheet, especially after the reverse repo facility is depleted or completely depleted that you will feel the full magnitude of QT." A lot of liquidity has been depleted from the system.

We might get an interest rate cut, but we can still be in a hawkish world because of the net liquidity drain of tightening.

With deflation/disinflation, there's an impact on workers' paychecks. No income at all is worse than deflation or disinflation.

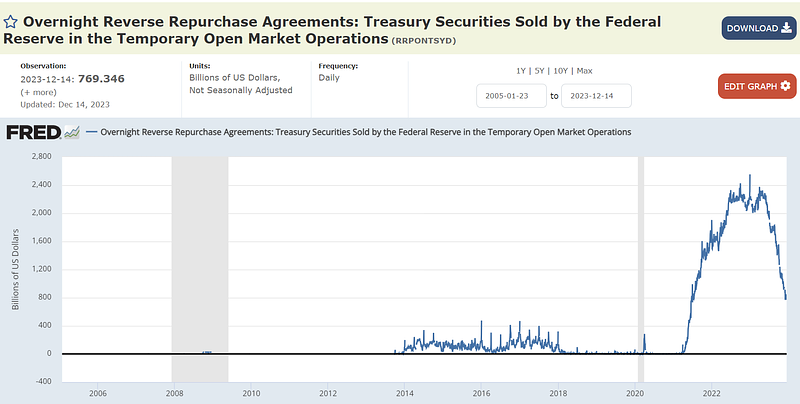

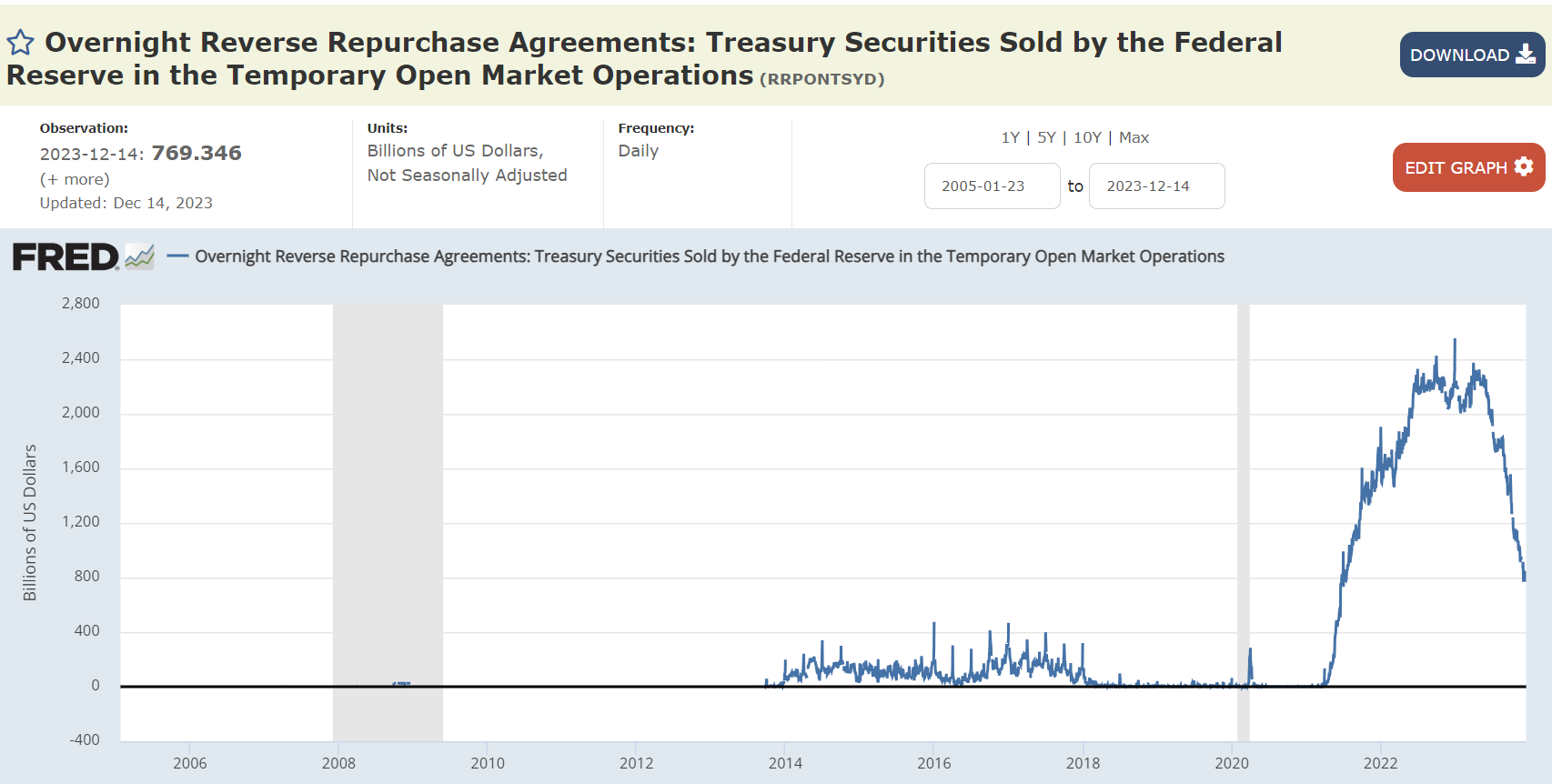

26:30 RRP facility - what happens when depleted? Explanation

When the Fed was raising interest rates, they were building up a "shock absorber". Banks did not want to get capital locked into Treasuries in an environment where rates were going up quickly. RRP allowed them to get a high yield close to Treasuries, but on an overnight basis (i.e. the capital doesn't get locked up).

As RRP depleted, the "shock absorber" gets thinner. With the Fed pause, banks are less concerned about the risk of rising interest rates. There may even be a risk of rates going lower, incentivizing banks to think about locking in current rates. So they are gradually using less of the overnight RRP facility and doing more buying of Treasuries directly.

Once that's "depleted" then Treasury bill sales will start to pull money out of the financial system (i.e. banking reserves will get "locked up" in Treasuries). It will be pulling dollars out of the system, effect on bank reserves.

Greenspud: I'm not sure if "depleted" is the best word to use, as so many financial commentators have been doing lately. "Depleted" to me suggests some form of scarcity, as if some aspect of the banking system is about to run out of money. I don't think this is the case since banks voluntarily participate in the ON RRP facility. What's happening is that it's just becoming a logical choice to park excess cash in other places than to use the ON RRP facility. Why can't that be viewed as a healthy thing? It's only during this most recent interest rate hiking cycle that use of the RRP facility has grown. During most other times it's under a low utilization, so this "depletion" is a return to normalcy.

I want to add George Gammon's relevant video questioning the relationships between bank reserves and stock market performance. From 2014 to 2019, bank reserves decreased, but the stock market went higher.

29:00 When will ON RRP be depleted? DDB: months, but not many months. About a quarter or two.

30:45 Wolf Richter - not confident that a recession will happen next year, but thinks it would be a good thing if it did happen. Recession part of the business cycle that gets rid of malinvestment.

It's important to note here that DDB stressed that she does not want to appear "insensitive" to the real economic pain that deflation brings to normal people.

32:00 Adam cites the Wolf Richter interview, questioning whether a recession is good for the economy overall. "Recession is a healthy part of the business cycle. It gets rid of the malinvestment. It keeps things from metastasizing... There's a real human cost that comes to recession and when natural market forces of deflation take over. But to a certain extent, maybe this is just the tough and needed medicine that we really need right now. If we could take the lumps but then get back to a more normalized business cycle, it would be better for everybody. If we could just demand it as a populace and embrace it as a group of elected leaders... if we want to have a better tomorrow we gotta tighten our belts and mutually sacrifice a little bit to let the malinvestment clear, but we will all be better off in just a couple years from this?"

Greenspud: My personal opinion on this is that it's easy to say that recessions are good if you are already in a well off financial position and can weather the storm. What's awful about recession is that the people hurt the most are hard working people who don't make enough money to have a comfortable savings buffer. Many of them are just young people who lack the experience for a high earning job and haven't had the time yet to build significant personal investments.

Older generations frequently criticize Millennials and Gen Z for "not getting" capitalism, but that resentment for our current economic system originates from the anxiety caused by working for fixed, low wages and then getting knocked down by hard economic times like this which they didn't have any control over. This has made it impossible for younger generations to achieve what used to be commonplace milestones like home ownership, car ownership, and starting a family.

Meanwhile, they notice corporate executives getting rich on the company's success, with compensation tied directly to metrics like profit and stock performance, none of which get shared with the employees. That's fine, but what happens in a recession is that those people at the top cash out early with piles of money and the fixed salary workers get screwed when the business goes under. So not everyone takes the "medicine" as Adam calls it, especially those who are responsible for the "malinvestment" that initially caused the problem.

I also wish the mainstream would quit pretending that we all blew our incomes on frivolous things like avocado toast! I am an Millennial and know nobody who eats avocado toast.

DDB praises "creative destruction" which ultimately builds stronger businesses that hire more people.

Many of the companies right now are so overindebted that insolvencies are bringing liquidations. You can say that liquidation is the most extreme form of creative destruction, but it is a much more destructive force on the economy and is harder on individuals against a backdrop of a Federal Reserve that hoovered up 1/3 of all mortgage-backed securities, leaving mobility very much impaired such that it's more difficult for American families to move to where tomorrow's jobs are in the current framework. Greenspud: I agree with DDB. I am stuck with my mortgage and moving from where I currently live would come at immense cost.

In this recession there will be "innocents" as opposed to speculators taken down. I agree with DDB also because with the current economic structure, the speculators don't get penalized when their risks blow up, but the employees they hired do.

39:36 - How much do you lie awake at night that we will have a Lehman moment before this is over?

Powell trying to push through regulations (Basel III) that will sever the lucrative link between the non-banking system ($250T) and the conventional banking system ($180T). It's not a coincidence that $JPM's business model is 75% capital markets. If we could push through regulations that effectively cut the oxygen off of the private capital market, then we would be so much better off for it in the end.

If you take away all the speculator's "toys", that's what Basel III endgame is. The "toys" only function in a 0% interest rate world with QE.

There's no stimulus check forthcoming before March 2025.

The inability to distinction between forms of stimulus it the "Achillies heel" for fintwit.

The form of fiscal stimulus matters most. If it's not money directly put into people's bank accounts, which stimulates inflation, it won't do much. Current Republican congress won't do it.

43:00 Despite tightening, Treasury has been hitting the gas pedal fiscally. DDB is saying don't count on that because of the divided congress - no stimulus.

No stimulus since September 14 when the employer retention credit has been put on hold. Infrastucture, CHIPS act, electric vehicle, etc - those stimulus efforts are not being directly given to households. They have to be distributed through the banking system.

Reverse Repo Facility is a different dynamic.

46:00 Powell - doing some unpopular things. i.e. enforce banking regulation - disappointing some powerful people. How much time does he have left?

Very difficult to fire him for cause. Precedent last set in late 1800s. Neither political party wants to filibuster. Fed Reserve Board would do everything to keep him in place so that future administrations can't just easily fire people. They would keep the chair in their place until SCOTUS rules whether or not its legal to remove a Fed chief for cause. Powell okay through 2026 when speaking constitutionally.

49:15 2024 market outlook

The quicker inflation falls, the more real real rates are. Interested in companies with a stable dividend. Asset class has really been beat down. Good balance sheet and commitment to dividend. 👍Continues to favor gold.

Nonfinancial investment to consider: family, start in sales, and take the course in college you don't want to take. The hardest class you can imagine - just do it.